As a sign that consumers continue to show greater confidence in the economy, credit card spending rose by nearly $16 billion during the third quarter of 2014 according to CardHub. Taking advantage of this momentum, 2015 represents an opportune time for credit unions with credit card programs to focus on growing their portfolios.

In the business of unsecured lending (credit cards in particular), underwriting is key. Effective underwriting facilitates two primary benefits: driving profitable loan growth and engaging members. In this article, we’ll focus on the following topics that contribute to a successful underwriting strategy:

- Developing stronger acceptance by saying Yes

- Maintaining continual credit line and re-pricing strategies for improved member engagement

- Implementing effective graduation strategies as your members’ needs evolve

Saying Yes’ To The Member

Optimizing the through-the-door acceptance and first-look approval rates go a long way toward ensuring success with any credit card program. There are many best practices at this stage. Here are some of the basics:

-

- Everything gets a second look. The original review of an application should leverage a comprehensive, properly developed scorecard. The scorecard is part of every financial institution’s DNA, made up of a combination of credit scores, payment histories, income verification metrics, etc. While the scorecard should help to quickly and efficiently identify the easy approvals, it makes sense to complete a manual review before denying any application.

-

- The more information, the merrier. Include supplemental information whenever possible, especially during the manual review process. Not all credit applications are cut-and-dried, so leveraging relationship information and other historic data points helps drive a credit decision that meet the applicant’s needs.

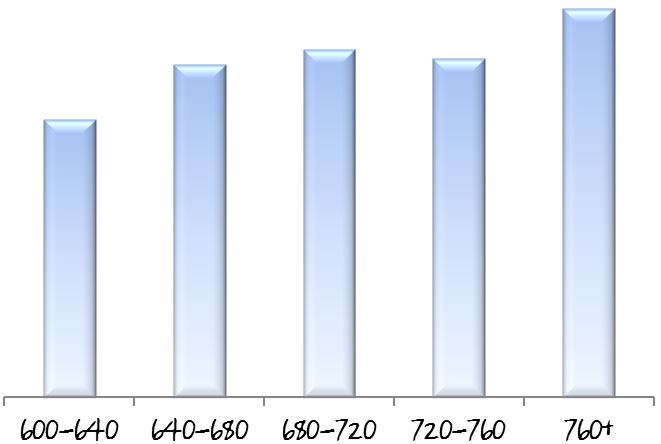

- Price for success. Having a multi-tiered risk-based pricing strategy is critical in the post CARD ACT world, given a more limited capability to adjust price in the future. This pricing strategy doesn’t mean you have to turn away from lower FICO bands. In fact, it should allow you to serve more members while maintaining an acceptable level of profitability within the lower tiers. For example, when looking at average profitability across select credit tiers for Elan’s credit union partners, you will find relatively stable levels of return, with only a marginal uptick in the higher credit tiers.

Chart 1. Return On Assets By Risk Score Range*

*Elan Financial Services proprietary data

By using the tools mentioned above, you’ll likely find opportunities to approve a higher percentage of applications. And keep in mind, many of the larger national issuers are more than happy to serve these near-prime members that were yesterday’s denials. Look for ways to say Yes to a member by offering a lower limit, a different rate, or an alternative product while ensuring your staff clearly understands the remedies available and how best to present them to your members.

Maintaining Member Engagement

Once you get the card into the member’s hand, credit line and pricing strategies play key roles in maintaining the relationship. Some significant tools in making this part of your underwriting a strategy a success include:

-

- Keep the pricing relevant. Members’ situations change over time, and a credit union cannot be slow to react to these changes. If a member’s profile strengthens over time, have a strategy in place to reduce the APR, potentially capturing more spending on larger-ticket items. Conversely, if you see negative trends in a member’s risk profile, don’t hesitate to protect your credit union by adjusting the price for future balances.

- Manage those lines. With credit line management programs, increases and decreases should be managed in a manner similar to APR. When members’ financial outlook improves, giving a line increase can enable them to use the credit card as a loan product for all of their needs, while your credit union captures additional balances. Meanwhile, line decreases are an effective way to nudge the cardholder toward more responsible behavior patterns.

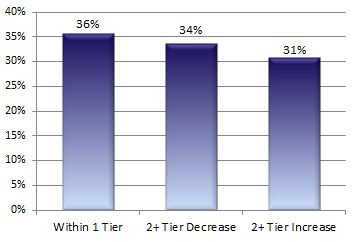

Managing ongoing cardholder engagement and risk represents one of the most difficult elements of an underwriting strategy, given the changing nature of members’ credit profiles. Elan sees this trend in its partners’ portfolios every day. For example, here’s the three-year FICO migration trend for cardholders initially booked with a 700-780 FICO.

Chart 2. Three Year FICO Migration Of Accounts With 701-780 FICO

Each tier represents about 20 FICO points.

Supporting Members’ Ongoing Needs

Presenting the right product to successfully acquire a new card account is just the beginning. In today’s competitive market, you must also continually refresh that product set to keep members in the fold. Some things to consider around products and product graduation include:

-

- Don’t overlook secured cards. These products represent an important first step, as they are a path for many of your members to enter or re-enter the credit card world, with an additional measure of safety and control. However, it’s important to view secured cards as a transitional step, having that next card available when members are ready to graduate to a more traditional product (low line, young adult, etc.). Establishing a proactive approach to reviewing these accounts (at 24 months on books, for example) helps maintain discipline in the process.

- Hang on to your affluent cardholders. Graduation strategies shouldn’t just be limited to those members on the lower end of the credit cycle. Over time, your traditional cardholders may qualify for the more affluent-focused cards, becoming prime targets for issuers who would love to pick up these high-value relationships. To remain successful, you must not only offer the right products to engage these higher-end cardholders, but recognize when it’s time to proactively upgrade within your existing card member base.

Lifecycle and product graduation strategies, though not directly related to product underwriting, carry significant influence in the long-term credit strategy. The specific product characteristics resulting from these strategies are what your members think of first when evaluating their current credit card relationship.

Long-Term Relevance Has Its Rewards

While you don’t strive to be all things to all people, it’s important to recognize the opportunities you may have to be a single-source provider for products and options that your members are currently getting from outside your credit union. As the credit card product is so closely tied to your members’ individual lifestyles and life stages, it’s a challenge to ensure each member’s card remains just as relevant and well-targeted year after year as it was the day it was booked. For that reason, credit card underwriting is not just a point-in-time activity; it’s an ongoing process. There’s a rewarding market out there for those who get it right.

For almost 50 years, Elan has delivered exceptional credit card products and service to its valued credit union partners. Today, Elan helps nearly 300 credit unions get credit cards into their members’ hands, utilizing the strategies mentioned above, along with many other industry-leading trends. Year after year, our partners remain pleased with the Elan solution, evidenced by a 96%+ renewal rate. For more information, call 1-800-223-7009 or visit www.cupartnership.com.