Auto lending is the bread and butter of the credit union loan portfolio. In fact, 5,797 credit unions, or 97.2% of the industry, held auto loans on their books as of third quarter 2016. But no two credit unions are alike, so it can be difficult for credit union executives to identify peers and share best practices for auto data benchmarking.

Broadening analysis to metrics other than growth is one way to help executives, staff, and board members better understand markets and the industry. In particular, data from the following five areas geography, seasonality, composition, total loan portfolio, and asset quality provides an in-depth examination of the auto portfolio.

1. Geography

Geographic factors can greatly impact a credit union’s auto loan portfolio. For example, consider the differences between a credit union with a footprint in Manhattan versus one in rural Wyoming. Factors such as population density and public transportation availability are important.

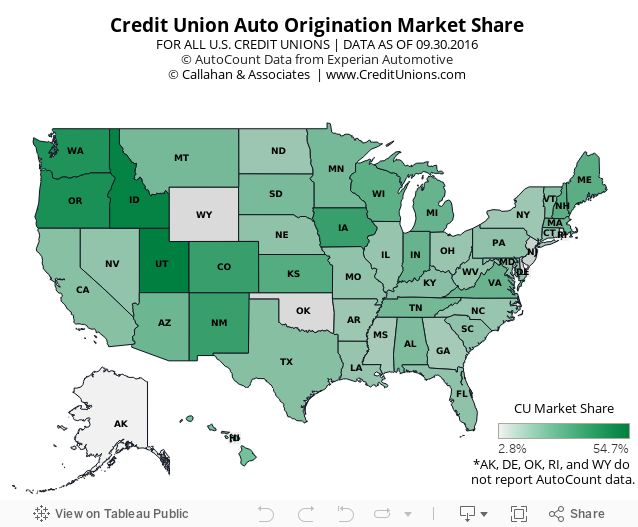

State trends also impact auto loan sales. Nationally, credit union auto loan origination market share is 17.8% year-to-date, but state figures vary considerably.

The color variation in the map below designates credit union market share the deeper the color green, the higher the market share. Hover over each state to compare third quarter data on market share, market size, and market growth.

var divElement = document.getElementById(‘viz1481224803902’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; vizElement.style.width=’642px’;vizElement.style.height=’569px’; var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

The market share for the two greenest states Utah and Idaho topped 50%. By contrast, the market share for New Jersey was 2.8%.

Even if other demographics are similar, how hospitable a state is to credit union auto lending can impact sales and financing.

Save Time. Improve Performance.

The data you need to better understand your auto portfolio is right at your fingertips. Build displays, filter data, and track performance of key auto metrics with Callahan’s Peer-to-Peer analytics.

2. Seasonality

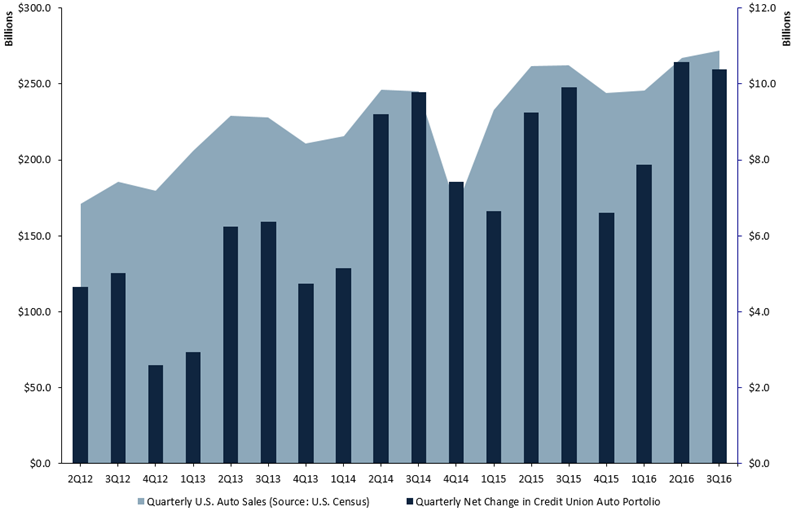

Consumers tend to purchase cars during the second and third quarter summer months. Likewise, auto lending, both on a national and credit union level, spikes in the second and third quarters. A strong third quarter might temp a credit union to project big auto numbers for the fourth quarter, but the seasonal nature of auto sales warns against this.

NET CHANGE IN AUTO LOANS

FOR U.S. CREDIT UNIONS | DATA AS OF 09.30.16

Source: Peer-to-Peer Analytics by Callahan Associates.

3. Composition

Understanding the composition of the auto portfolio and the related trends isn’t just helpful for the lending team, it’s helpful for front-line staff, too. An all-around educated credit union staff is better equipped to serve members’ needs and identify opportunities for the institution.

And composition is also a good way to measure a portfolio’s performance.

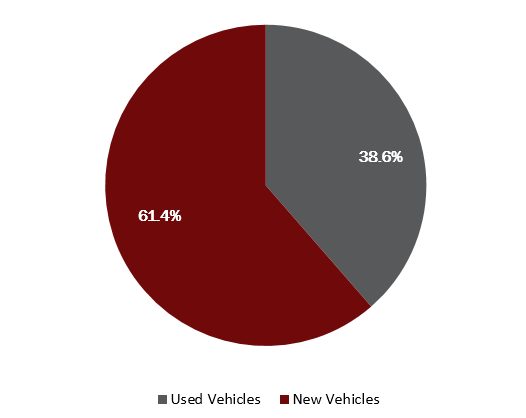

For example, at 61.4%, used auto loans accounted for the largest part of the auto portfolio in third quarter 2016. That follows with the historical composition of the credit union auto portfolio. However, new auto loans have been growing in composition share. New auto loans accounted for 38.6% of the auto portfolio as of third quarter 2016 that’s up 70 basis points from third quarter 2015.

AUTO LOAN COMPOSITION (NEW VS. USED)

FOR U.S. CREDIT UNIONS | DATA AS OF 09.30.16

Source: Peer-to-Peer Analytics by Callahan Associates.

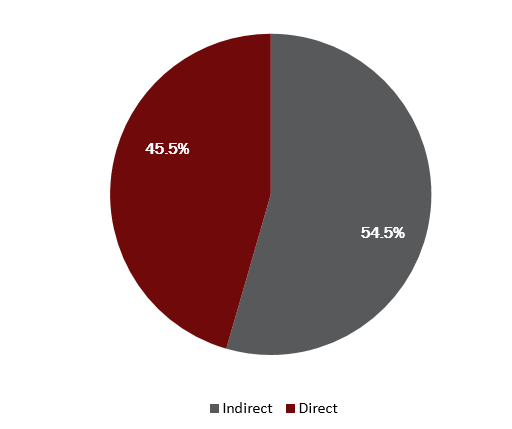

Another composition element to consider is the breakdown of direct and indirect lending. Currently, indirect auto loans comprise 54.5% of the industry’s auto loan portfolio. But in the third quarter of 2012, indirect loans comprised 43.3% of the composition. This composition continues to change, so it is important to monitor.

AUTO LOAN COMPOSITION (DIRECT VS. INDIRECT)

FOR U.S. CREDIT UNIONS | DATA AS OF 09.30.16

Source: Peer-to-Peer Analytics by Callahan Associates.

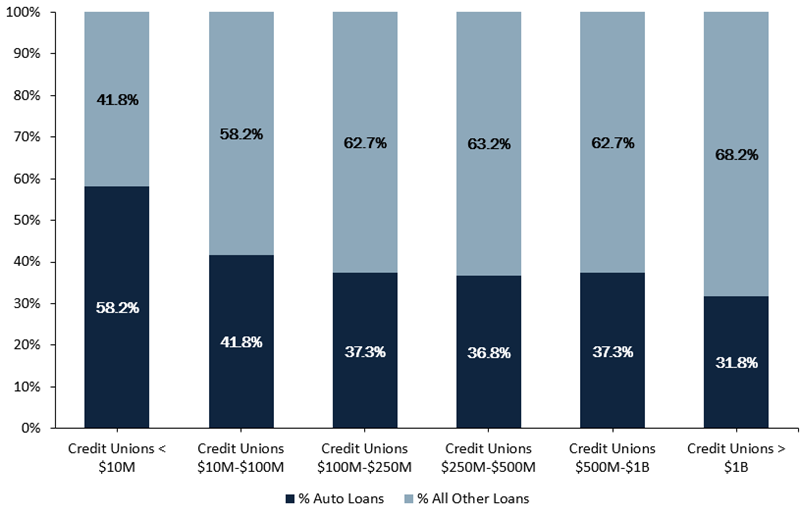

4. Percent Of Loan Portfolio

Understanding the importance of auto loans in the credit union’s overall loan portfolio can shed light on possible opportunities and risk.

The industry average for auto loans as a percentage of total loans is 34.2%. That figure is representative of the aggregate credit union market, but it does not capture what is happening in different asset bands.

There’s a clear difference between credit unions with less than $10 million in assets and those with more than $1 billon. Auto loans makeup 58.2% of the loan portfolio for the former group, whereas they makeup only 31.8% of the loan portfolio for the latter group.

Benchmarking against similarly sized asset-based peers is especially helpful for this metric.

AUTO LOANS AS A PERCENTAGE OF TOTAL LOANS

FOR U.S. CREDIT UNIONS | DATA AS OF 09.30.16

Source: Peer-to-Peer Analytics by Callahan Associates.

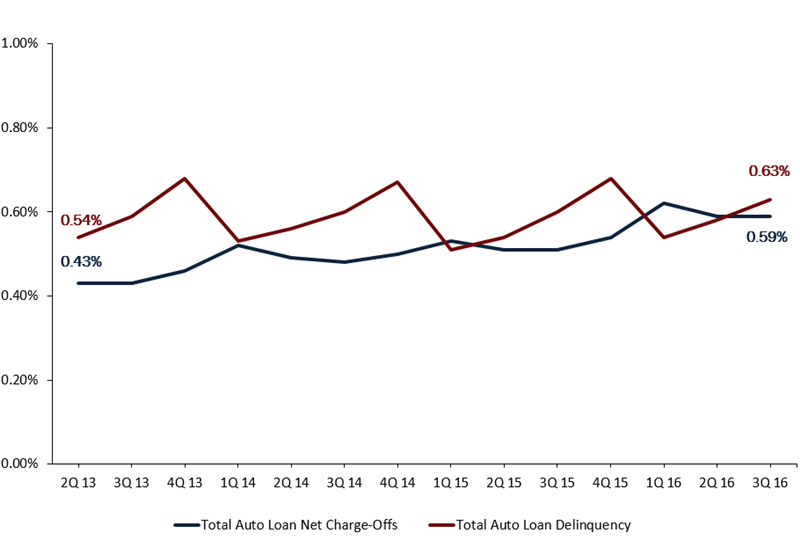

5. Asset Quality

Analyzing auto delinquency and net charge-offs is especially important when a credit union is considering ramping up or scaling back auto lending or evaluating the impact of indirect lending.

The industry’s total auto delinquency rate was 0.63% as of third quarter 2016 with a 0.40% rate for new autos and 0.77% for used. Since NCUA started reporting it in second quarter 2013, total auto delinquency has stayed within the 0.51% and 0.68% range. The total auto net charge-off ratio was 0.59%, down from its record 0.62% high in the first quarter of 2016.

AUTO LOAN NET CHARGE-OFFS AND DELINQUENCY

FOR U.S. CREDIT UNIONS | DATA AS OF 09.30.16

Source: Peer-to-Peer Analytics by Callahan Associates.

The goals and strategies to manage asset quality can be at odds with those used for increasing auto loans, so examining what’s happening at the industry level can offer needed perspective.

As demonstrated, many factors color the performance of credit union auto lending. So this quarter, consider different metrics to gain a better understanding and add context to conclusions and decisions.