Top-Level Takeaways

-

Community First members are saving $30,000 more a month by rounding up debit transactions.

-

The credit union plans to digitize enrollment to remove friction from the registration process.

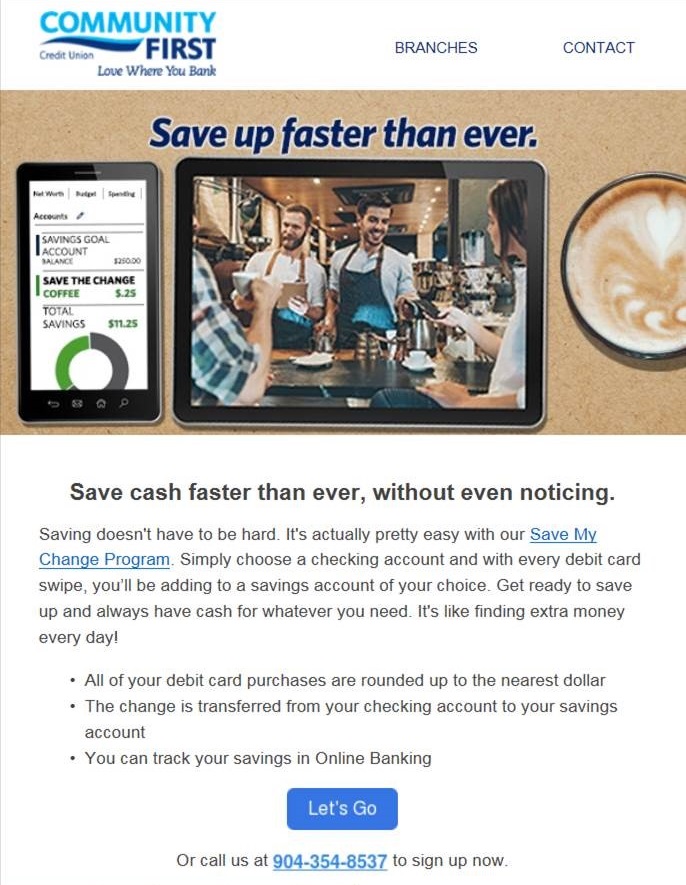

A year-old debit swipe and savings plan at Community First Credit Union of Florida ($1.6B, Jacksonville, FL) offers financial wellness for members and additional income for its own bottom line.

The north Florida credit union launched Save My Change in October 2017. The opt-in program rounds up a member’s debit transactions to the nearest dollar and deposits those pennies and nickels and dimes into a savings account.

“Such programs have been around for some time” says marketing vice president Roger Rassman, “but Community First offers a twist.”

“We have purpose-based savings accounts available” Rassman says. “Members can name the account with their goal in mind, like a new car or a down payment on a house or education savings.”

Members can easily track their progress on an app that displays the goal, the account balance, and individual transactions.

First Community members who sign up for the program increase their debit transactions per month from approximately 25 to 32, according to Rassman. That translates to roughly $2.50 more per account per month in interchange income. With 2,000 members enrolled, that’s $5,000 a month in additional income.

“More importantly” Rassman says, “members are socking away an average of 50 cents per debit swipe. At 30 or so debit transactions per month on average, that’s an additional $15 per member and $30,000 in total savings for all members per month.”

“The financial wellness piece is the driving reason for offering Save My Change” Rassman says, “and it’s a piece of Community First’s work with the Center for Financial Services Innovation. Savings is one of the weakest areas for our membership. But it’s also one of the things we can easily work on. An automated program like this is appealing to people, especially millennials now aging in the workforce and looking for ways to save.”

Although Rassman calls the program a no-brainer for the credit union, there is still some work it needs to do on execution. For example, there is little friction from the perspective of the credit union it deposits savings from the swipes by batch every night but getting started in the program is not so easy for members.

“Members have to interface with a human being, either in a branch or over the phone, to enroll” Rassman says. “Or, they can fill out a web form and someone will contact them. And as part of their workflow, our people ask about this when opening accounts. We promote it quarterly by email and other ways to existing members, but we need to make the process more frictionless.”

One side benefit of that friction is that members have to also engage with a human being to unenroll, but Rassman doesn’t see that happening much.

“We’re not matching deposits, so there’s no good reason for people to jump in and out of this” the marketing vice president says.

In other words, it’s easy to do nothing and keep saving money after that initial signup. And digitizing the enrollment is on the docket for first quarter 2019.

“We know we can fix that, and we plan to” Rassman says. “That will get even more members participating.”

This interview has been edited and condensed.