Maximizing the ROI of a limited budget is a daunting task many credit union marketing executives face. In 2013, Northern Federal Credit Union ($226.7M, Watertown, NY) began analyzing member accounts to identify borrowing behavior and uncover opportunities among members with less than A+ credit.

We were losing auto loans to dealerships, says Alexa Bennett, marketing manager for Northern FCU. We wanted to show members the value of maintaining a loan with us over these higher cost indirect lenders.

So the credit union, which does not operate an indirect lending program, initiated an ACH auto loan recapture program that brought in nearly $2.2 million in additional auto loan business in 2016.

Mining ACH Data

CU QUICK FACTS

Northern FCU

DATA AS OF 09.30.16

HQ: Watertown, NY

ASSETS: $226.7M

MEMBERS:29,173

BRANCHES:7

12-MO SHARE GROWTH:7.6%

12-MO LOAN GROWTH:7.4%

ROA: 0.53%

Bennett knew Northern had member bill payment data available in its core systems, but she wasn’t sure exactly how to extract or use the information.

During a strategic planning meeting with lending and retail staff in 2013, the group discussed a source of business intelligence the credit union was currently using. It came from soft credit pulls for loans and new accounts from which Northern learned about member borrowing patterns.

We already were applying the relationship banking model to find new business opportunities and offer members our products using other vendors’ data, Bennett says.

But could the credit union create a straightforward, low-cost, high return marketing strategy based on its own data?

We wanted to show members the value of maintaining a loan with us over these higher cost indirect lenders.

The prospect of mining business data for marketing possibilities intrigued Bennett, who started looking deeper into the core.

We could see what loans they were paying from accounts here, says the marketing manager. I was sure we also could see how much they were paying to whom and create marketing promotions from that.

As she examined the data, it was evident Northern’s ACH data was the key to tapping this market; however, Bennett didn’t have the business intelligence software to run reports and pull targeted ACH data from the core.

So, Bennett’s challenge became how to extract ACH data cost-effectively.

Strategic Marketing On A Lean Budget

Bennett’s fiscal position is not unknown to credit union marketing managers.

Marketing budgets are contingent [upon results] and can be trim, Bennett says. We have to show the worth of the dollars invested every single time.

DO YOU KNOW YOUR NUMBERS?

Manually tracking marketing returns can be time-consuming, but with Callahan Analytics, it only takes a few minutes to see how you compare against peers. Stay ahead of the game. Contact us to see Callahan Analytics in action.

For this campaign, we had to determine how to allocate those dollars to extract our ACH data and create a marketing campaign to recapture auto loans, Bennett explains.

Market segmentation and target marketing became critical and, initially, Northern focused on members paying off auto loans from another lender.

The credit union leveraged the direct marketing services of its core processor, which offers data mining and targeted marketing services to other credit unions. However, according to Bennett, Northern was the first credit union to ask about a campaign based on an auto loan payment reduction scenario.

I asked to run a report to find members borrowing from particular national and local lenders with minimum loan balances of $10,000 or who’d paid their Northern auto loan off in the previous 90 days, Bennett says. I got back more than 3,000 members who fit my criteria.

Northern FCU uses Synergent for its core processing. Find your next solution in the Callahan & Associates online Buyer’s Guide.

Using those names, Bennett launched an ACH loan campaign in late second quarter 2016.

Surprising Insights In Phase One

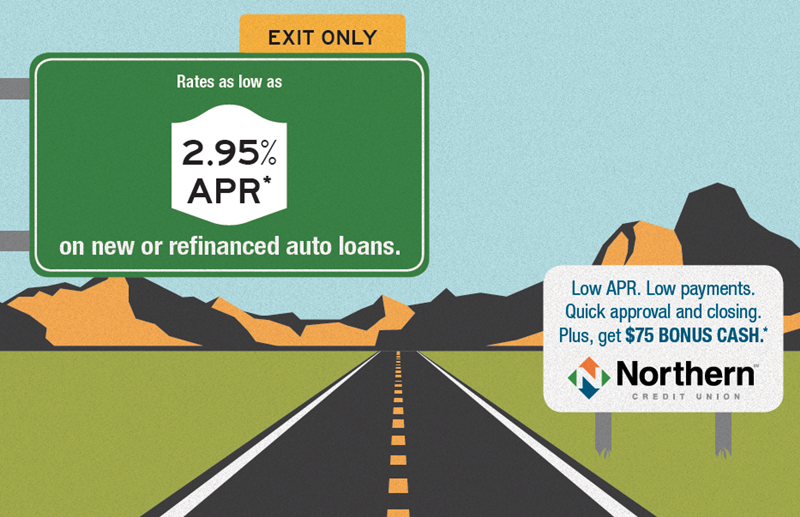

As part of the campaign, Northern created a postcard that featured a diminutive dog and a compelling offer. It presented recipients with a customized payment scenario based on borrowers of a similar profile, offered rates beginning at 2.95% APR, and showed what a lowered payment amount might be.

Northern Credit Union used its core provider to mine ACH data and identify ideal members for an auto recapture campaign. Click here to view the campaign postcard.

We wanted members to think, This loan is X dollars, but mine is higher at Y, so I could save this amount monthly if I refinance with Northern, Bennett says.

The promotion also offered the convenience to apply by phone or online, terms up to 72 months, no payments for 30 days, and a $100 gas gift card.

The promotion was a hit with members bringing in 63 new loans and slightly more than $920,000 in new and refinanced auto loans, according to the credit union.

Northern reports the average loan from the campaign is 4.5 years at 7% APR, and the credit union estimates it will earn $104,498 in interest during the first two years. The total campaign cost $7,610 and generated $14 generated for every $1 dollar spent, according to Bennett. All told, the campaign paid for itself in two months.

And Northern gained other surprising insights from the campaign.

Quite a few a few people who weren’t right for new auto loans wanted other credit products like signature loans, Bennett says.

Member Appreciation In Phase Two

Recognizing these member needs, Northern launched its second ACH marketing campaign in the fourth quarter of 2016.

The credit union promoted another auto refinancing as well as cash bonus incentives for other credit products, such as credit cards, home equity loans, lines of credit, and mortgages.

For Northern’s second ACH data-based campaign, the credit union looked beyond auto financing to products such as credit cards, HELOCs, and mortgages. Click here to view the campaign postcard.

Year-end is when members make resolutions like getting into financial shape, Bennett says. This campaign gave us the chance to build better relationships with members by talking through their other financial needs.

The fourth quarter promotion garnered nearly $1.3 million in new or refinanced auto loans for the credit union and cost only slight more than $5,000 to produce, Bennett says.

According to Northern, the average loan from the second campaign is 5.39% APR for 60 months. And the credit union estimates it will earn $115,563 in interest during the first two years. Its ROI was nearly 64% higher $22 per $1 spent than for the first promo.

More significantly, the credit union’s focus on attracting additional credit business paid off.

Don’t reinvent the wheel. Get rolling on important initiatives using documents, policies, and templates borrowed from fellow credit unions. Pull them off the shelf and tailor them to your needs. Visit Callahan’s Executive Resource Center today.

Northern closed 60 signature loans totaling $420,281 with full-term interest income equaling $73,683. It also opened three home equity lines of credit totaling $120,600 with full-term interest income minus incentives equaling $10,287 as well as nine credit cards for $85,500 in line value.

These results, and the new member relationships that developed, got our staff excited, Bennett says. Staff learned all they had to do after building rapport with members was ask for the business. Because members appreciate how much we care about their financial futures, they’ll say yes.’

CLICK ON THE TABS BELOW TO LEARN ABOUT NOTHERN FCU’S PERFORMANCE

AVERAGE LOAN BALANCE

Northern FCU’s average loan balance per member is notably higher than credit unions in its asset band or state.

YOY GROWTH OF AVERAGE MEMBER RELATIONSHIP

Strategies like the ACH loan campaign at Northern FCU have helped the New York cooperative form deeper relationships with members.

RETURN ON ASSETS

Northern Federal Credit Union’s ROA has steadily improved since the first quarter of 2013, and campaigns to maximize advertising dollars supplement this trend.

$(‘.collapse’).collapse()

Key Takeaways And Future Plans

According to Bennett, it’s important with this target market to have a flexible approach and avoid taxing credit union resources.

We decided cash bonuses were better to avoid getting calls about gift cards, for example, she says.

Also, because many members had older or lower value cars, Northern lowered the required auto loan minimum to $7,500 from $10,000.

We still wanted to help those members, Bennett says. For many, saving $100 a month on their car loans makes a real difference.

Finally, Bennett discovered other credit products might be more valuable to members, as auto loans aren’t their only need. So, she’s looking forward.

We want to expand our ACH loan recapture program to mortgages, student loans and credit cards, she says. I want to do these campaigns twice yearly with separate promotions for each credit type.