CU QUICK FACTS

Jeanne D’Arc Credit Union

Data as of 03.31.18

HQ: Lowell, MA

ASSETS: $1.4B

MEMBERS: 85,269

BRANCHES: 11

12-MO SHARE GROWTH: 3.9%

12-MO LOAN GROWTH: 13.5%

ROA: 0.96%

Jeanne D’Arc ($1.4B, Lowell, MA) is a low-income designated credit union based in Lowell, MA, a blue-collar, former factory town known as the cradle of the American Industrial Revolution.

But the community-chartered credit union’s field of membership extends beyond the borders of the historic mill town. For that reason, Jeanne D’Arc serves working-class communities like Lawrence and Leominster in Massachusetts and Nashua in New Hampshire as well as white-collar areas like Harvard, Lunenburg, and Lancaster in Massachusetts.

Given the scope of demographics, it’s not surprising that the economic realities of Jeanne D’Arc’s members likewise differ. What might be more interesting is that the credit union believes this doesn’t have to be the case.

We try to move people from low-to-moderate income into middle-to-upper income,’ says credit union CEO Mark Cochran. We provide services to help members take the next step, wherever they are in their financial life.’

To do this, the credit union focuses on two areas: financial education, and lending and saving. ContentMiddleAd

Financial Education

The term financial education’ has become a buzzword among credit unions, says Anne Marie Sousa, Jeanne D’Arc’s vice president of marketing and financial education. But the Bay State cooperative has been making inroads in that arena for more than a decade.

Financial education is a hot topic, but it’s not new for us,’ Sousa says. We kicked off our efforts 13 years ago.

Back in 2005, Lowell Public Schools received a grant through the U.S. Department of Education to establish an after-school program. The students needed help with math concepts, so the program coordinators reached out to Jeanne D’Arc for help. Sousa built a curriculum in which self-paced reading, lectures, and activities supported lesson plans that contained clear goals and objectives.

We teach the same concepts they are already learning, but in a different way,’ the VP says. We try to be more fun. And since we aren’t school employees, they tend to pay a little bit more attention.

BEST PRACTICE: Ditch The Attention Deficit

Instead of adopting a canned, lecture-based program, Jeanne D’Arc builds its own financial wellness lessons to accommodate the needs of different audiences and hold the attention of kids who learn best by doing.

The credit union’s foray into financial education piqued the interest of other area programs and services. First came calls from the high schools, elementary schools, and preschools. Then came the outreach from senior centers and special needs programs.

To meet the demand, Jeanne D’Arc created a financial education department that now includes a staff of four employees three financial education specialists plus a manager as well as Sousa. All are certified educators of personal finance.

The team’s financial education specialists focus on one of three age groups pre-kindergarten to fourth grade, fifth to eighth grade, and high school. All three teach college students and adults.

The group creates its own teaching content but does borrow questions and concepts from canned programs like CUNA’s Mad City Money. Subject matter and concepts are largely similar across age groups, but educators present the information differently depending on the audience. For example, middle schoolers learn about budgeting via different colored Skittles, whereas students of Lowell and Dracut high schools attend reality fairs hosted by Jeanne D’Arc.

Jeanne D’Arc has been teaching financial education at area schools for more than a decade. Here, financial education specialist Gratia Gosselin uses Skittles to teach budgeting to middle school students.

The financial education team also runs the credit union’s Save at School program. Twice a month, specialists visit 20 local elementary schools to collect deposits from students and stress the importance of saving.

We tell them, You have a habit of brushing your teeth and doing your homework. You need to make a habit of saving money, whether it’s what you got for your birthday or the nickel you found on the street,” Sousa says.

Additionally, the credit union leads financial education workshops at area workplaces, runs three in-school branches at local high schools, and offers 24 financial wellness modules on topics ranging from loan approvals to emergency savings via its website MoneyStrong.org, which is part of Jeanne D’Arc’s larger MoneyStrong program.

In 2017 alone, Sousa says the credit union reached more than 19,000 people across more than 500 classes.

But Jeanne D’Arc doesn’t just look externally for opportunities to improve financial wellness. Last year, the credit union surveyed its own employees to gauge their financial wellness across MoneyStrong’s 24 modules. It then offered resources for employees who wished to learn more.

We surveyed them again in February and saw improvement in every single category,’ Sousa says.

We’re a smaller shop trying to do our best. We’re showing them our trust, and they’re responding.

Click the tabs below to view graphs.

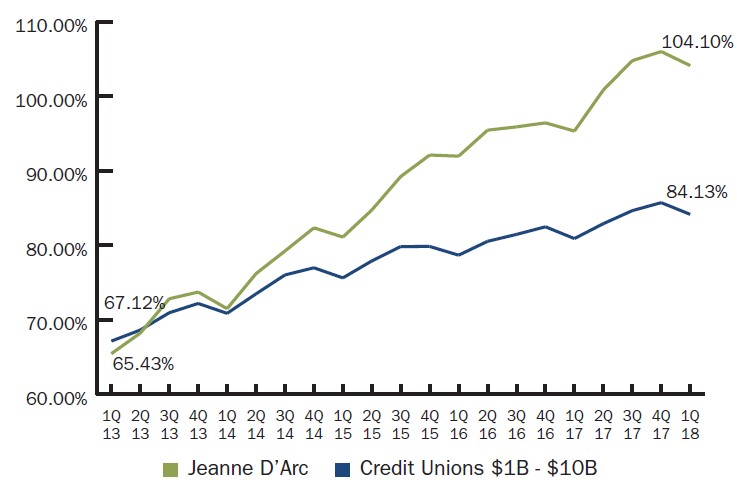

LOAN-TO-SHARE RATIO

LOAN-TO-SHARE RATIO

FOR U.S. CREDIT UNIONS $1B-$10B | DATA AS OF 03.31.18

Jeanne D’Arc’s first quarter loan to share ratio of 104% was nearly 20 percentage points higher than the average of similarly sized institutions.

Source: Callahan Associates.

TOTAL DELINQUENCY AND NET CHARGE-OFFS

TOTAL DELINQUENCY AND NET CHARGE-OFFS

FOR U.S. CREDIT UNIONS $1B-$10B | DATA AS OF 03.31.18

The credit union’s total delinquency and net charge-off rates 0.46% and 0.19%, respectively bested the asset-based peer averages of 0.57% and 0.48%. For Jeanne D’Arc, this portfolio performance highlights member loyalty to the cooperative.

Source: Callahan Associates.

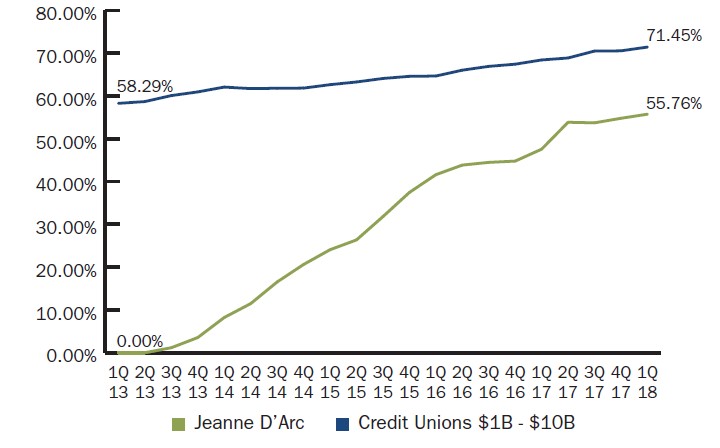

INDIRECT LOANS / TOTAL AUTO LOANS

INDIRECT LOANS / TOTAL AUTO LOANS

FOR U.S. CREDIT UNIONS $1B-$10B | DATA AS OF 03.31.18

To retain borrowers at the point of sale, Jeanne D’Arc stepped into indirect lending in 2013 through a CUSO, Indirect Auto Solutions. As of first quarter 2018, indirect lending comprised more than 55% of the credit union’s auto loan portfolio.

Source: Callahan Associates.

MEMBER VALUE

MEMBER VALUE

FOR U.S. CREDIT UNIONS $1B-$10B | DATA AS OF 03.31.18

| Rank | State | Name | Total ROM Score |

|---|---|---|---|

| 1 | IA | Veridian | 97.27 |

| 2 | IA | University of Iowa Community | 93.98 |

| 3 | WI | Altra | 92.83 |

| 4 | MI | Lake Michigan | 92.78 |

| 5 | ID | Idaho Central | 91.82 |

| 6 | CA | Firefighters First | 91.66 |

| 7 | PA | Citadel | 90.83 |

| 8 | NY | Bethpage | 88.33 |

| 9 | WI | Royal | 87.95 |

| 43 | MA | Jeanne D’Arc | 73.79 |

With a ROM score of 73.8, Jeanne D’Arc came in at No. 43 among the 288 credit unions with $1 billion to $10 billion in assets. Callahan’s Return Of The Member (ROM) provides a comprehensive scoring system of member value.

Source: Callahan Associates.

EFFICIENCY RATIO

EFFICIENCY RATIO

FOR U.S. CREDIT UNIONS $1B-$10B | DATA AS OF 03.31.18

Over the past five years, Jeanne D’Arc has lowered its efficiency ratio approximately 20 percentage points to 69.2%. It nearly matched its peer average in the first three months of 2018.

Source: Callahan Associates.

AVERAGE MEMBER RELATIONSHIP

AVERAGE MEMBER RELATIONSHIP

FOR U.S. CREDIT UNIONS $1B-$10B | DATA AS OF 03.31.18

As of first quarter, Jeanne D’Arc’s average member relationship was $23,800. That was higher than the $21,000 average of credit unions with $1 billion to $10 billion in assets and the $19,400 average of credit unions in Massachusetts.

Source: Callahan Associates.

Lending And Saving

The MoneyStrong initiative at Jeanne D’Arc Credit Union takes a holistic approach to financial wellness. It offers community workshops and in-school programs to improve the financial education of everyone it touches. It also offers savings and lending products designed for those who struggle to save money.

We’re in a working-class, blue-collar community,’ says Brian Sousa, Jeanne D’Arc’s senior vice president and chief lending officer. That’s the impetus behind this.’

On the savings side, the credit union’s signature deposit product is a savings account that pays 7% APY on balances up to $500. And if these members need credit, Jeanne D’Arc also has a suite of loan products designed for folks who either don’t have credit or need help repairing it.

Loans include credit cards, autos, and unsecured products, and provide greater benefit for current members of the credit union. Members with credit scores between 619-639 are eligible for a one-time rate reduction of 50 basis points for the life of the loan if they make on-time payments for the first 12 months. Members who qualify for a MoneyStrong credit card receive automatic limit increases.

Financial struggles can be cyclical, and Jeanne D’Arc recognizes the value in providing assistance to get members going again.

Everyone goes through cycles,’ says Paul McDonald, vice president of residential and consumer lending. We’re a smaller shop trying to do our best. We’re showing them our trust, and they’re responding. They would do everything to reciprocate our trust.’

That’s what the numbers say, too. As of first quarter 2018, Jeanne D’Arc’s total delinquency of 0.46% was 12 basis points lower than the average for credit unions with $1 billion to $10 billion in assets. Its 0.19% net charge-off rate bested its asset-based peer group’s average by 30 basis points.

BEST PRACTICE: Trust Loyal Members

The hard-working, loyal nature of Jeanne D’Arc’s members means the credit union can go out on a limb to help those with damaged credit or no credit at all. The cooperative’s vice president of residential and consumer lending admits the credit union makes loans his previous community bank employer wouldn’t have, and that’s OK.

In addition to overseeing the credit union’s loan program, the lending team administers two educational efforts of its own designed to help members along their financial journey.

Once every year, Jeanne D’Arc holds credit workshops in which attendees, typically 20-40 per session, receive advice from an independent credit expert. Jeanne D’Arc runs individual credit reports and provides one-on-one credit counseling.

The credit union also holds first-time homebuyer seminars throughout the year at its headquarters. It brings in real estate agents, attorneys, and other experts to walk attendees, typically 40-50 per session, through the process. Attendees earn a $500 credit toward closing costs.

Jeanne D’Arc doesn’t serve solely members of low-tomoderate means, but its efforts in this area are an important part of the organization’s focus. From promoting financial education in schools to developing products for the credit challenged, Jeanne D’Arc teaches members how to be better stewards of their financial futures. Financial health is a lifelong commitment, and Jeanne D’Arc is committed to helping members live well.

Anatomy Of Jeanne D’Arc Credit Union

This article appeared as part of Callahan’s Anatomy Of A Credit Union series. Read more in the Jeanne D’Arc series today.