Top-Level Takeaways

-

RBFCU is in the second phase of its lending and operational response to the coronavirus pandemic.

-

After broadly approving requests for help, it now requires proof of financial hardship from members.

-

Lending service teams learned new skills in different areas as they pitched in, creating a new culture of cooperation in the process.

The lenders at Randolph-Brooks Federal Credit Union($10.8B, Universal City, TX) are in phase two of helping as many of its nearly 900,000 members as possiblecope with the financial fallout of the coronavirus pandemic.

Heather Sullivan, SVP for Consumer Lending, Randolph-Brooks FCU

The first phase began March 17 with skip-a-loan payments on consumer loans and credit cards and forbearances and similar provisions for mortgages and commercial loans.

Phase two, which includes the final wave of branch lobby re-openings, began June 8. The biggest difference for phase two lending relief comes in the form of availability.

Although the first round of consumer lending assistance was broadly available, the second phase requires proof of financial hardship, says Heather Sullivan, RBFCU’s senior vice president for consumer lending.

Sullivan says the focus now is on the entire lending relationship, and the big cooperative’s collections department is currently reviewing requests.

They do an overview of the member’s financial hardship and determine what modifications can be made to the existing loans that will allow the member to continue managing their financial obligations, Sullivan says. This mightinclude additional skips, extension of term, or conversion of open lines of credit to a closed-term loan.

From Broad Outreach To Fine-Tuning

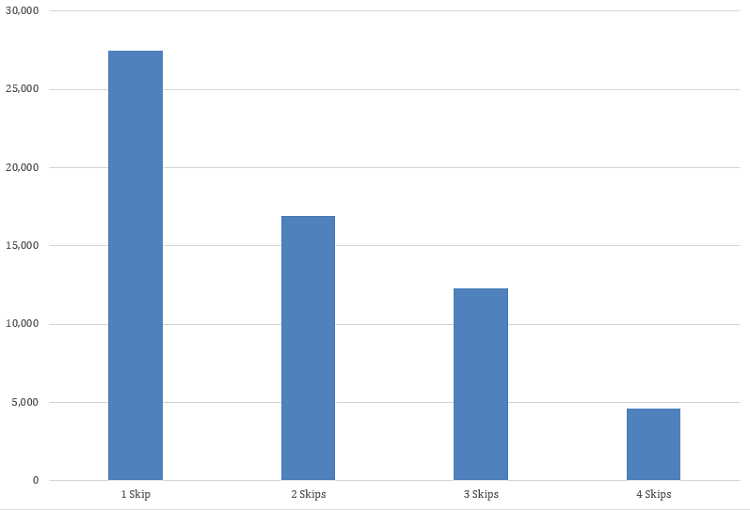

According to Sullivan, as of last week, RBFCU has allowed 27,479 consumer loans to skip one payment, 16,927 loans to skip two, 12,253 loans to skip three, and 4,580 loans to skip four payments. In April alone, the credit union reset rates on 236 loansand reduced the average payment by 17%.

LOANS AND SKIPPED PAYMENTS

FOR RANDOLPH-BROOKS FCU | DATA AS OF 06.08.20

Callahan & Associates | CreditUnions.com

RBFCU has allowed 27,479 consumer loans to skip one payment, 16,927 loans to skip two payments, and 12,253 loans to skip three payments.

We had a broad outreach and didn’t try to fine-tune the audience, Sullivan says of the first phase. Members whose personal budgets might not be impacted could well be helping family and friends that were.

The credit union is taking a more proactive approach for the second phase, however.

We’re now engaging with members through email notifications, starting with those who have three skips on their loans, since they’re the ones who seem more likely to have been financially impacted, Sullivan says.

Refine your credit unions response to COVID-19 using the Ideas In Action: Pandemic Response page, a hub for all of our articles, webinars, and policies concerning the COVID-19 outbreak.

Flexing Virtual Muscles

Responding to the sudden needs of thousands of members required RBFCU to develop its ability to serve people virtually and efficiently, flexing the virtual muscles the enterprise had already been developing.

We had made a lot of advancements the past few years that expanded how members could interact online to complete the lending process, Sullivan says. This allowed us to continue lending and filling members’ needs without havingbranches available.

According to Sullivan, RBFCU closed 49.3% of its direct auto loans and 58.7% of its personal loans in January through DocuSign. In April, with branch lobbies closed, those numbers jumped to 96.8% and 95.8%, respectively.

Ease of use made adapting to an online process less stressful for members, says Sullivan, who has been with RBFCU for 22 years and in charge of consumer lending for the past three. They were thankful we had options available to meettheir needs.

Of course, there are people behind that digital prowess, and many on the RBFCU staff found themselves suddenly developing new skills in new roles.

When it came to member service, all our lending shops worked together to keep the channels flowing, Sullivan says.

All Hands On Deck

RBFCU has a diverse set of member service teams among its workforce of approximately 2,100 full-time equivalent employees.

That includes the 150-agent member service center, a 130-agent consumer lending call center, and a mortgage call center and commercial call center that usually have 10 and five agents working, respectively.

Sullivan says the credit union quickly trained up 10 employees from her consumer lending team to answer mortgage or commercial calls when wait times became excessive. Her employees joined a group of 20 from the member service center who also added mortgagecalls to their normal duties. And, because lobbies were closed, branch staff also joined in. They, too, had to learn some new skills, a process that also put the big cooperative’s technology to the test.

We had a reservist program set up that kept branch staff trained to take member service center calls but had never used more than one employee per branch before, Sullivan says. We learned quickly we needed more licenses to deployall the support that was available in the branches, and we coordinated with IT to make those adjustments.

8 Ways To Achieve Nirvana

Heather Sullivan, senior vice president for consumer lending at Randolph-Brooks FCU, offers eight best practices she says RBFCU has learned and leaned on as it moved from phase one into phase two of its pandemic response.

- Lean on the team. Teamwork, which I consider a strength for RBFCU, reached a higher level. Everyone across the organization came together. We used one other’s strengths and various solutions from our individualareas to overcome challenges.

- ABC: Always be communicating. The open communication and quick problem-solving was remarkable. We spoke about workflows and where things were bottlenecking. This allowed individuals to relate issues to their world,and that’s where we identified solutions that had been used for similar instances.

- Strive for nirvana. Share the vision of what would be the nirvana outcome. You can make allowances if there’s limited time to solidify the solution, but if people don’t understand what you want to create,you’re limiting the possibilities.

- Flex and adapt. Stay flexible and be ready to adapt as new truths are realized.

- Experiment and ask for help. Don’t be afraid to try things and ask for help. The staff enjoyed getting involved in other processes and getting to know different people in the organization.

- Help can come from the outside. Include your vendors in overcoming challenges. They might have a solution or another credit union that could help.

- Test. Test. Test. Ensure strong quality control. The validation after go-live helps to identify anything that wasn’t thought about or solved for, so you can correct it quickly.

- Express gratitude. Enough said.

Cross-Training For Member Fitness

All those different teams had to educate members on what options they had available, guide them through the online application process, answer simple questions, and sometimes route members to other departments, such as specialized mortgage areas, Sullivansays.

Without licensing, this team was not able to answer complex questions, the lending executive adds. But, being able to provide the members their options, set expectations, and submit requests for follow-up contacts allowed the mortgageteam to focus their attention on processing the applications.

Much the same process occurred with the sudden flood of Paycheck Protection Program loan applications.

Facilitating the quick role transition relied on first providing the teams answers to easy questions and guidance on each program, then having 15- to 20-minute calibrations each morning, Sullivan says. In those sessions, leaders updatedthe staff on the FAQs they were using, provided feedback, and gave a pep talk for the day.

A Cohesive Team

After two weeks, the synergy was solid and the calibration sessions were limited to once a week and then phased out as the assistance was no longer needed, Sullivan says.

RBFCU will take what it has learned the past several months and apply it beyond simply routing a loan deferral or other transactional requirement. For the credit union, the biggest learning has surrounded team development.

We learned how much support we have in one another, and the staff feedback has been very positive, Sullivan says. They feel secure and appreciated knowing all the things we’re doing to serve members and keep employees safe whilewe all adapt to an evolving work environment.