Throughout the fourth quarter, many state governments expanded pandemic restrictions as fears surfaced surrounding the new Omicron variant. Even so, consumers spent at pre-pandemic levels through the second half of the year.

Record savings balances and seasonal holiday purchasing activity supported increased spending. This change, coupled with an absence of federal relief, helped to drive down the average personal savings rate to 7.9%, which is well below the high of 26.6% recorded in March 2021 and more in line with pre-pandemic levels. Although liquid deposit account growth remains strong at financial institutions, the slowdown is a welcome relief from the operational pressures faced during the past 18 months.

Key Points

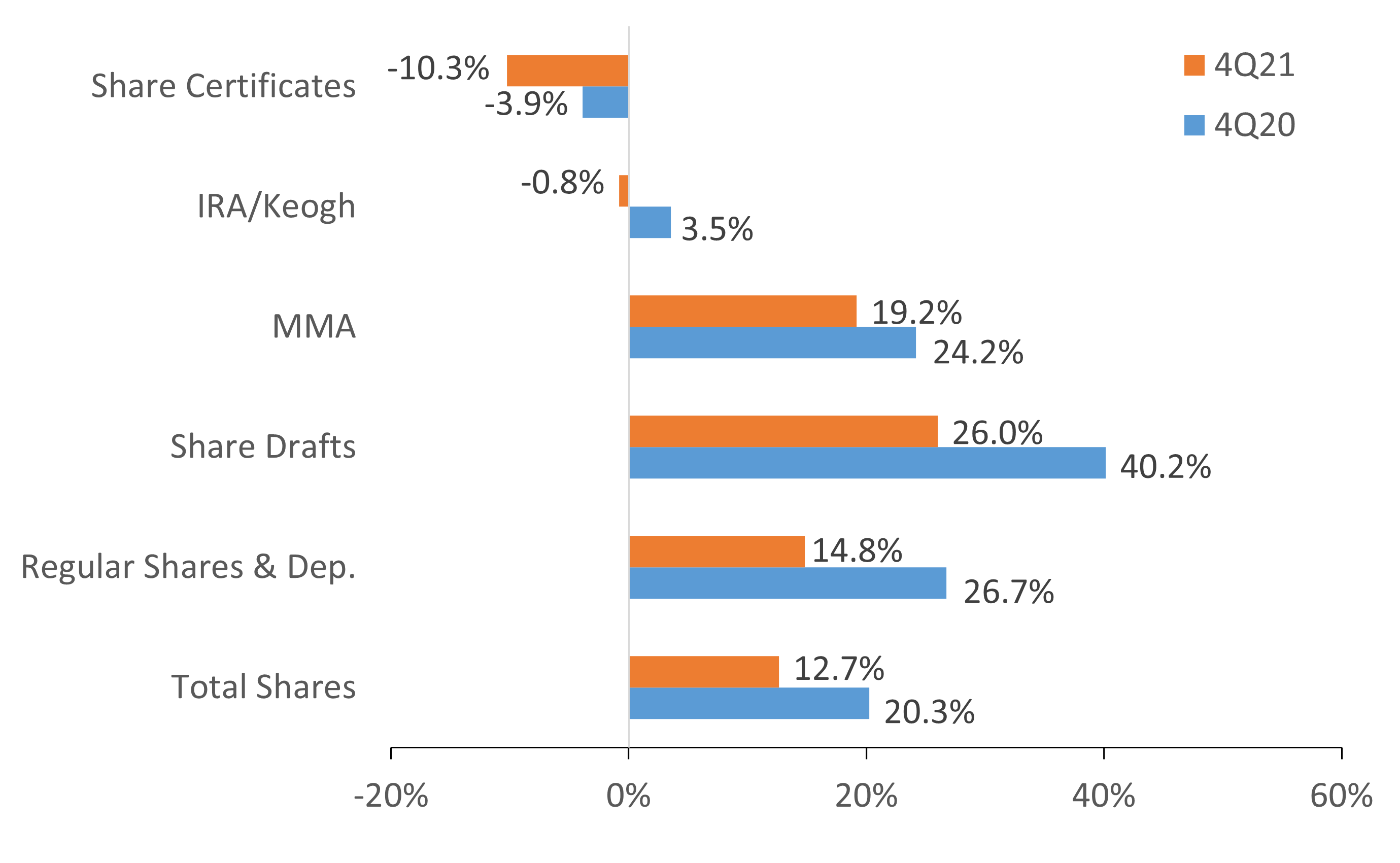

- Total share balances increased 12.7% annually to over $1.8 trillion as of Dec. 31. Quarterly share growth of 2.3% in the fourth quarter exceeded both second and third quarter share growth rates but lagged loan expansion.

- Share draft balances grew 26.0% annually, the fastest rate of all major deposit products. Share draft penetration increased 94 basis points year-over-year to a record 61.2% as more members turned to credit unions for their transactional accounts.

- Share certificate balances fell 10.3% annually, continuing the termed product purge from credit union balance sheets that began in early 2020. IRA Keogh account balances also declined 0.8% in 2021, the largest calendar-year contraction since the first quarter of 2014. Easy access to funds is still a member priority.

ANNUAL SHARE GROWTH BY TYPE

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.21

Callahan Associates | CreditUnions.com

Growth decelerated in share products across the board in 2021, slowing marginally in each quarter of the year. Liquid core deposit products continue to be the top choice for members.

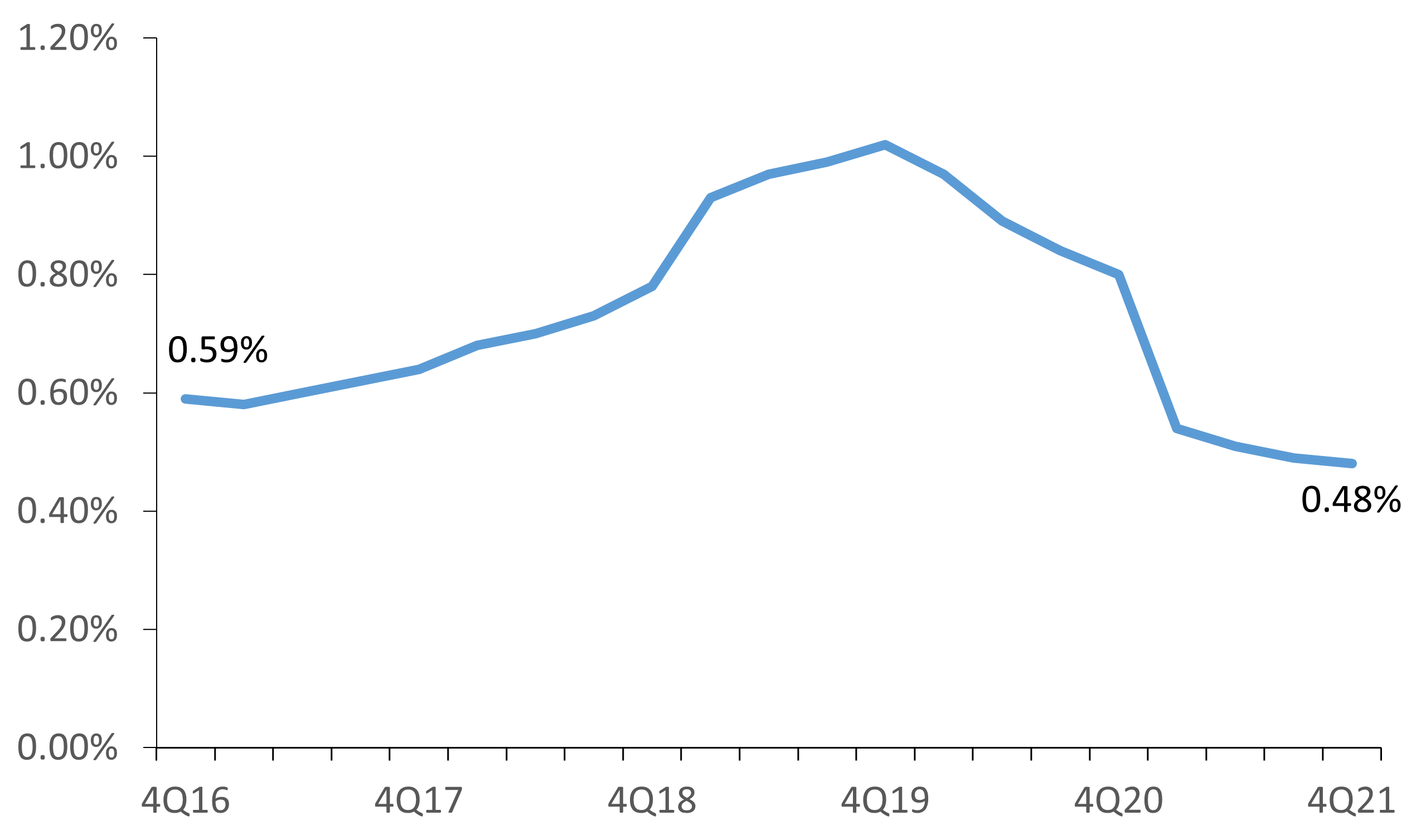

AVERAGE COST OF FUNDS

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.21

Callahan Associates | >CreditUnions.com

The average cost of funds reached a record low following eight straight quarters of decline, thanks to a member preference for low-dividend deposit accounts.

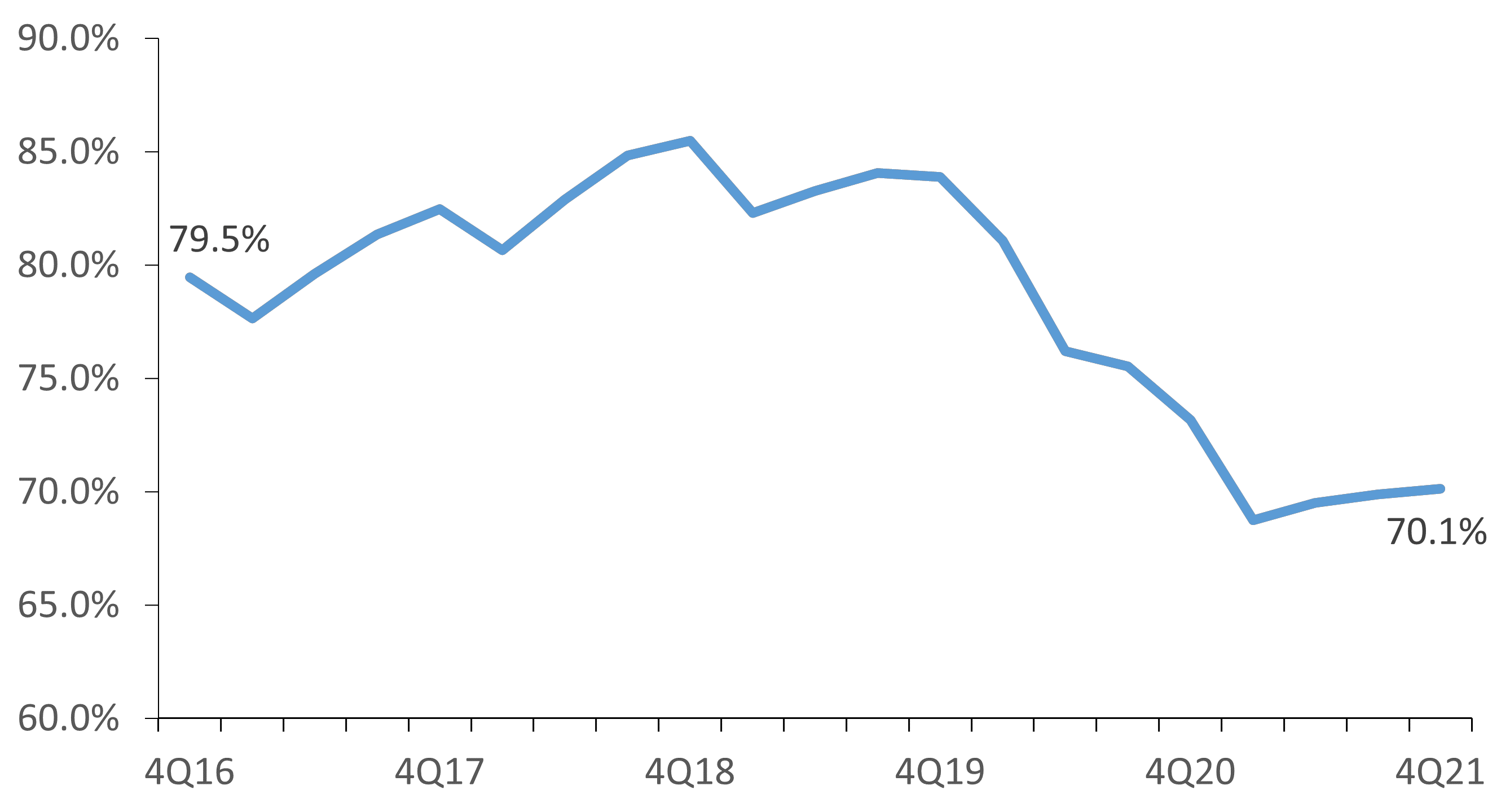

LOAN TO SHARE RATIO

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.21

Callahan Associates | CreditUnions.com

The loan-to-share ratio ticked up in each quarter of 2021, as federal relief slowed. Lending growth has now outpaced share growth for the third consecutive quarter.

The Bottom Line

Share portfolio growth remains healthy at credit unions nationwide. The portfolio topped $1.8 trillion for the first time ever more than double a decade ago. Unprecedented fiscal and monetary stimulus drove millions of dollars into member share accounts in 2020.

Although deposits are still flowing in at a healthy clip, slowing growth in 2021 indicates a general return to conventional deposit flows and gives credit unions time to repurpose some of these new shares into productive loans in 2022. Cooperatives and members are starting to stabalize loan and share relationships into a new post-pandemic equilibrium.

Click the topics below to read more analysis from the fourth quarter of 2021.

|

AUTO |

EARNINGS |

HUMAN CAPITAL |

|

INVESTMENTS |

LOANS |

MACRO |

|

MEMBER RELATIONSHIPS |

MORTGAGES |

SHARES |