Non-interest income is a source of stability and success for credit unions, but how can financial cooperatives maximize non-interest income without raising service fees for members? One way is through other operating income.

The NCUA defines other operating income as dividends from the NCUSIF, income or loss derived from selling real estate loans on the secondary market, interchange income, interest income earned on purchased participations not qualifying for true sales accounting under GAAP, unconsolidated CUSO income, and the adjustment to carrying value of loans used as the hedged item in a fair value hedging designation.

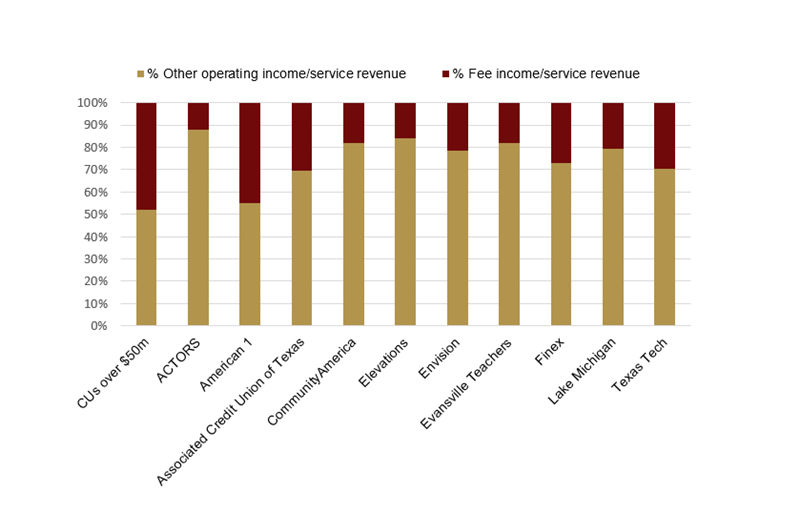

The following 10 credit unions lead those with more than $50 million in assets in annual other operating income as a percent of total assets.

LEADERS IN OTHER OPERATING

For all U.S. credit unions > $50 million in assets | Data as of 12.31.15 Callahan & Associates | www.creditunions.com

| Rank | State | Name | Other Operating Incom / Assets | Other Operating Income | Assets | Members |

|---|---|---|---|---|---|---|

| 1 | FL | Envision | 4.74% | $13,942,348 | $293,937,086 | 33,812 |

| 2 | NY | ACTORS | 3.61% | $7,780,580 | $215,316,774 | 23,815 |

| 3 | MO | CommunityAmerica | 3.11% | $64,794,028 | $2,084,177,049 | 198,536 |

| 4 | CT | Finex | 2.75% | $2,176,364 | $79,095,359 | 10,173 |

| 5 | IN | Evansville Teachers | 2.59% | $28,947,909 | $1,116,457,371 | 130,508 |

| 6 | TX | Associated Credit Union of Texas | 2.58% | $8,390,610 | $325,825,662 | 35,078 |

| 7 | TX | Texas Tech FCU | 2.39% | $2,689,974 | $112,584,239 | 13,099 |

| 8 | MI | Lake Michigan Credit Union | 2.22% | $84,732,944 | $3,814,957,444 | 270,750 |

| 9 | CO | Elevations | 2.22% | $34,203,105 | $1,542,433,257 | 114,378 |

| 10 | MI | American 1 | 2.17% | $6,124,521 | $281,592,050 | 53,536 |

Source: Peer-to-Peer Analytics by Callahan & Associates

In terms of what contributes to the leaders’ exceptional other operating income, these credit unions have higher than average investments in credit union service organizations (CUSOs) and first mortgage loans sold to the secondary market. This combinationunderpins their other operating income, allowing these credit unions to post increases in non-interest income without raising fees. In fact, this group of leaders reports a 3.7% decrease in fee income over assets year-over-year.

Follow The Leader

Explore dozens of leader tables and hundreds of pages of credit unionperformance data in Callahan’s Credit Union Directory. It’s the gold standard for reliable insight. Read the digital download today.

Explore dozens of leader tables and hundreds of pages of credit unionperformance data in Callahan’s Credit Union Directory. It’s the gold standard for reliable insight. Read the digital download today.

Leading Commonalities

It is important to note the leaders posted the highest operating income-to-assets ratio in all the industry while still posting year-over-year growth in assets in 2015. The average asset growth among the 10 leaders was 11.3% compared to an average of7.2% for credit unions with more than $50 million.

The leaders also posted higher than average performance in other operating income as a percentage of total service revenue calculated by adding fee income and other operating income. The group average for this metric was 79.7% versus 52.12% forall credit unions with more than $50 million in asssets.

Finally, the 10.71% average member growth rate at these 10 credit unions more than doubled the 4.7% average for all credit unions with more than $50 million in asssets.

SERVICE REVENUE COMPOSITION

For U.S. credit unions >$50 million in assets | Data as of 12.31.15Callahan & Associates | www.creditunions.com

Source: Peer-to-Peer Analytics by Callahan & Associates

Non-Interest Income

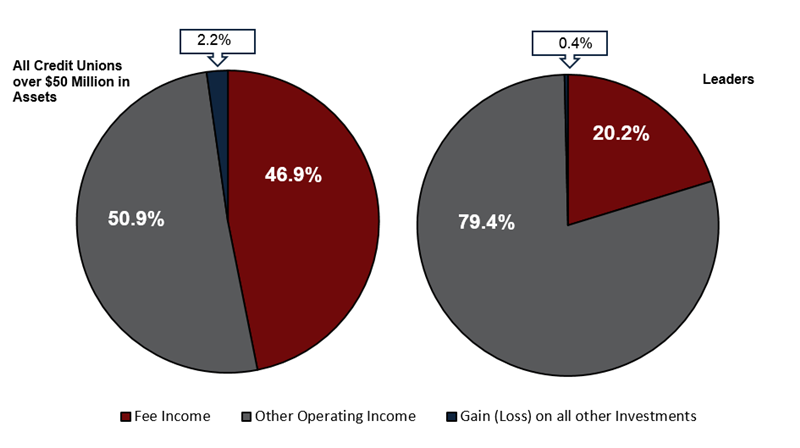

The percent of non-interest income to assets remains in the range of 1.3% for credit unions with more than $50 million in assets; however, fee income as a proportion of non-interest income has been shrinking annually.

Fee income as a percent of non-interest income for credit unions with more than $50 million in assets is down from 50.4% in December 2014 to 47.9% in December 2015, which is still higher than the average posted by the 10 leaders above.

Other operating income comprises 79.4% of non-interest income for the leaders and 50.9% for credit unions with more than $50 million in assets.

NON-INTEREST INCOME COMPOSITION

For U.S. credit unions >$50 million in assets | Data as of 09.30.15

Callahan & Associates | www.creditunions.com

Source: Peer-to-Peer Analytics by Callahan & Associates

Increasing service fees might seem like a simple way to grow non-interest income, but there are complicating factors, not to mention members, to consider. The Consumer Financial Protection Bureau is planning to curtail overdraft protection fees, whichmight cause a drop in non-interest income. Consequently, credit unions would do well to look to other operating income to increase non-interest income, as the leaders noted here have done.

You Might Also Enjoy

- Leaders In Average Member Relationship Growth

- State In The Spotlight: Alabama

- Leaders In SBA Lending

- The Dynamics Of The Loan-To-Share Ratio