With 5,959 institutions reporting representing 99.4% of industry assets the second quarter of 2016 is on track to be another record-breaking one for the credit union industry. Loan balances topped $834 billion, a 10.7% annual increase, and credit unions broke the previous record of $809 billion set in first quarter 2016.

The increase in loan balances was primarily driven by first mortgages and used and new auto loans. Together, they accounted for 81.6% of total loan growth over the past year.

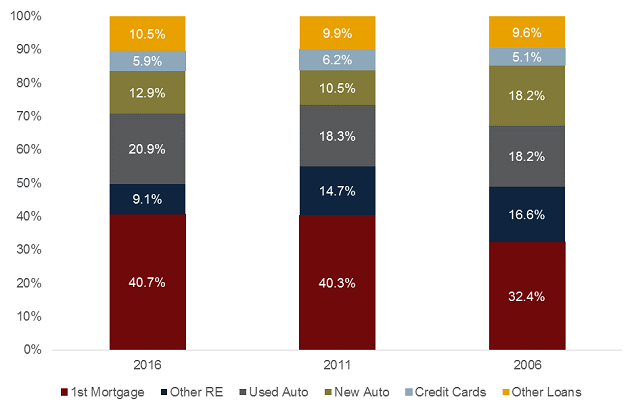

LOAN COMPOSITION

For U.S. credit unions* | Data as of 06.30.16

Callahan Associates | www.creditunions.com

Source: Peer-to-Peer Analytics by Callahan Associates

*For 5,959 credit unions

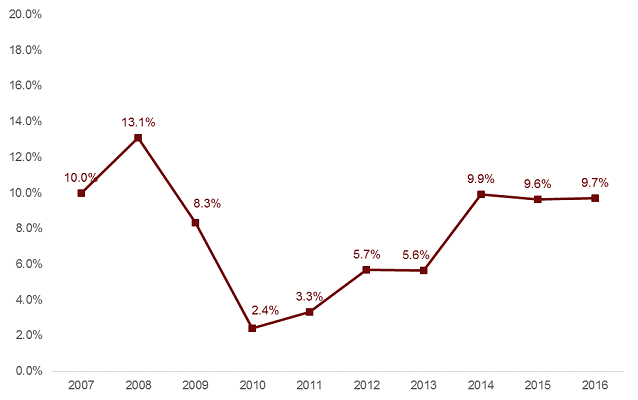

1. First mortgages increased 9.8% annually and accounted for 37.6% of total loan growth.

Credit unions now hold more than $340.7 billion in first mortgage loans, the highest ever reported balance. Originations in the first six months of 2016 totaled $62.6 billion, a 1.7% annual increase over the previous June, and the most loaned since June 2013.

FIRST MORTGAGE GROWTH

For U.S. credit unions* | Data as of 06.30.16

Callahan Associates | www.creditunions.com

Source: Peer-to-Peer Analytics by Callahan Associates

*For 5,959 credit unions

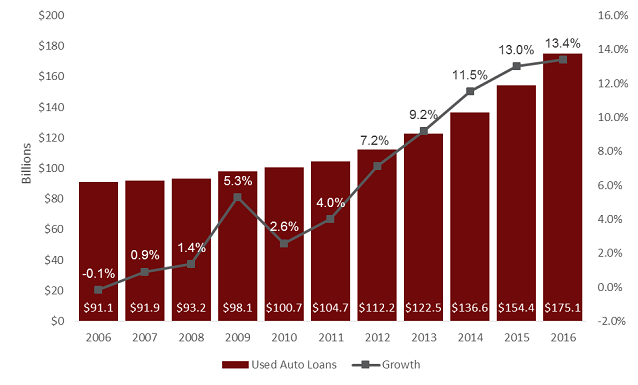

2. Used auto loans increased 13.4% year-over-year and topped $175.1 billion in June 2016.

Used auto balances at credit unions rose $20.7 billion from June 2015 to June 2016, accounting for 25.8% of total loan growth over the past year. Used auto loans comprise 61.8% of the auto loan portfolio and yield an average loan balance of $11,941.

USED AUTO LOAN BALANCES AND GROWTH

For U.S. credit unions* | Data as of 06.30.16

Callahan Associates | www.creditunions.com

Source: Peer-to-Peer Analytics by Callahan Associates

*For 5,959 credit unions

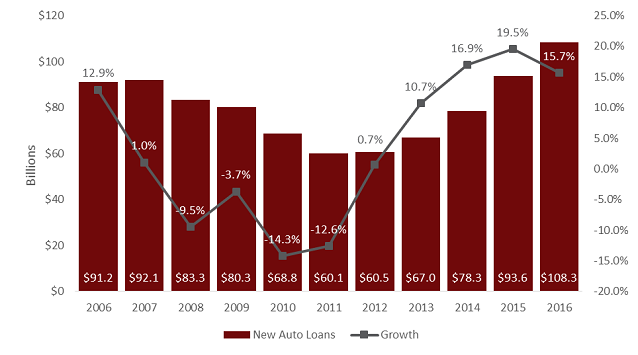

3. New auto loans increased 15.7%, adding $14.7 billion to the loan portfolio over the past 12 months.

New auto loans account for 18.4% of total loan growth over the past 12 months, increasing $20.7 billion year-over-year and adding 572,550 new auto loans to the portfolio. The average new auto loan balance was $19,719 as of second quarter. That’s a 3.6% jump over June 2015, when it was $19,030.

NEW AUTO LOAN BALANCES AND GROWTH

For U.S. Credit Unions* | Data as of 06.30.16

Callahan Associates | www.creditunions.com

Source: Peer-to-Peer Analytics by Callahan Associates

*For 5,959 credit unions

BE SMART. ATTEND TRENDWATCH.

This must-attend quarterly event for credit union leaders covers performance trends, industry success stories, and areas of opportunity. Attendees will find insight they won’t find anywhere else weeks before the official NCUA data release.