First quarter investment trends largely followed preceding quarters with some additional variance due to normal seasonality. Liquidity pressures have persisted amid sustained strong loan demand, although growth in loan balances has gradually slowed for the past several quarters. Deposit inflows were stronger than expected. As a result, credit unions diverted excess liquidity to the investment portfolio.

From an earnings perspective, credit unions posted significant growth in investment income compared to preceding periods. The flattening yield curve and the subsequent shift in the composition of the investment portfolio toward shorter maturity products has contributed to increase in yields.

As credit unions look ahead to the remainder of 2019, there are a few key points to keep in mind.

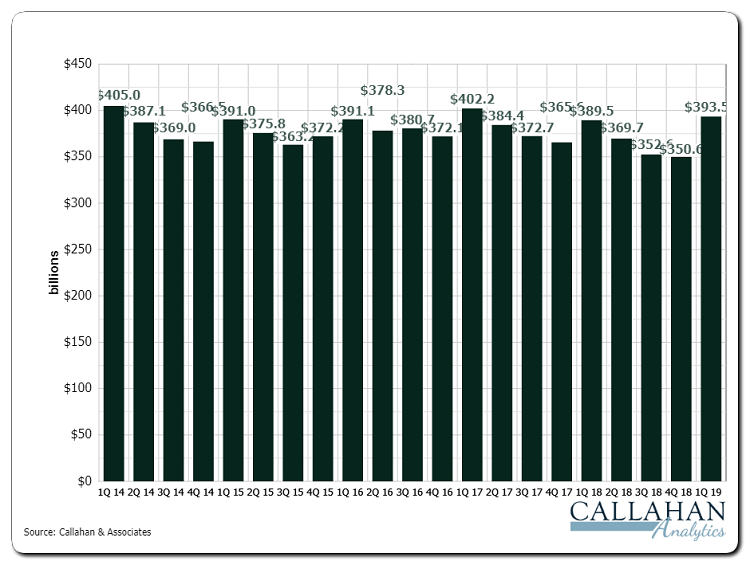

Total Investments

As of March 31, 2019, credit unions held $393.5 billion in investments. That’s up 12.2% quarter-over-quarter the largest quarterly increase since the third quarter of 2009 and up 1.0% year-over-year. The rise in total investments is consistent with historical cyclicality, with first quarter balance growth largely a byproduct of strong deposit inflows.

Share balances followed a similar trend, increasing 4.5% from last quarter and nearly 6.0% from last year. With more than half of the annual deposit growth from share certificates, credit unions are increasingly seeking avenues to attract deposits and remain competitive.

Balance sheet growth remained healthy, with total credit union assets up 3.7% quarterly and 6.5% year-over-year. Overall loan portfolio growth, although strong, continues to slow. Quarterly loan balances rose 0.6% from December 2018 and 8.0% from March 2018.

TOTAL INVESTMENTS

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.19

Callahan & Associates | CreditUnions.com

Largest quarterly increase in balances since March 2009.

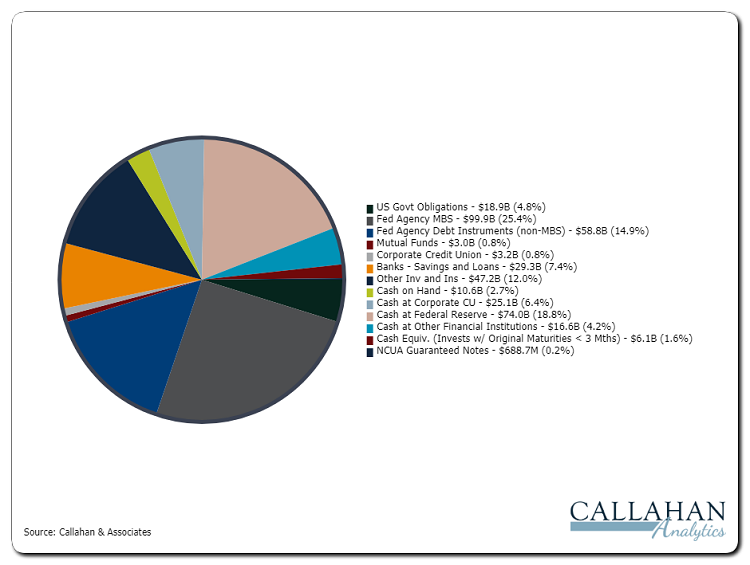

Investment Composition

Cash and investment balances grew $42.9 billion in the first quarter to $393.5 billion. This was largely the result of increased investments to overnight accounts at both the Federal Reserve and corporate credit unions as well as short-term cash equivalents and federal agency MBS products.

As of the first quarter of 2019, credit unions are required to report overnight investment balances at the Fed in a newly created line item on the 5300 Call Report. In total, credit unions reported balances of $74.0 billion at the Fed as of March 31, nearly $13 billion above the previously aggregated category (cash at other financial institutions) where credit unions reported Fed balances in prior quarters. Cash at corporate credit unions surged 47.3% or $8.1 billion from year-end 2018 to $25.1 billion. The segment’s share of the investment portfolio increased 1.5 percentage points.

The combination of strong first quarter deposit inflows, a relatively flat yield curve, and continued liquidity pressures from sustained loan demand has led credit unions to keep excess liquidity in overnight products. Beyond growth of corporate cash, mutual fund balances posted the second-largest percentage gain from the fourth quarter of 2018. In total, mutual fund investments increased 19.8% since year-end, continuing a recent upward trend after hitting a low in December 2015.

INVESTMENT COMPOSITION

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.19

Callahan & Associates | CreditUnions.com

Fed and corporate cash balances rise.

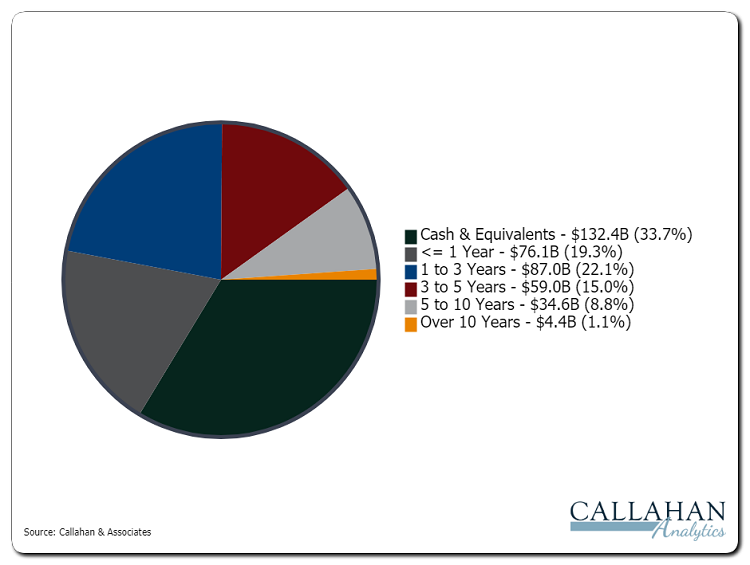

Investment Maturity

Maturities of investment portfolios at U.S. credit unions shifted in the first quarter of 2019, with balances of both short and long investments growing from the fourth quarter and one year ago. Cash and equivalents posted the largest increase in the portfolio, growing 41.3% on a quarterly basis, rising from $93.7 billion last quarter to $132.4 billion as of March 31.

As a result, this segment’s share of the portfolio rose 6.9 percentage points, largely due to the increases in Fed and corporate cash balances while investments in products maturing in one to three years and three to five years contracted 0.3% and 2.0%, respectively from year-end 2018. Conversely, investments in securities maturing in five to 10 years and greater than 10 years expanded as well, increasing 8.9% and 9.0%, respectively. Given the substantial growth in cash and equivalents, the percentage of the portfolio allocated to investments less than three years rose 2.5 percentage points to 75.1%. Looking ahead, with growing uncertainty around future rate increases in 2019, credit unions are staying short to minimize risk and remain nimble for future liquidity needs.

INVESTMENT MATURITY

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.19

Callahan & Associates | CreditUnions.com

Investments move toward shorter maturity products.

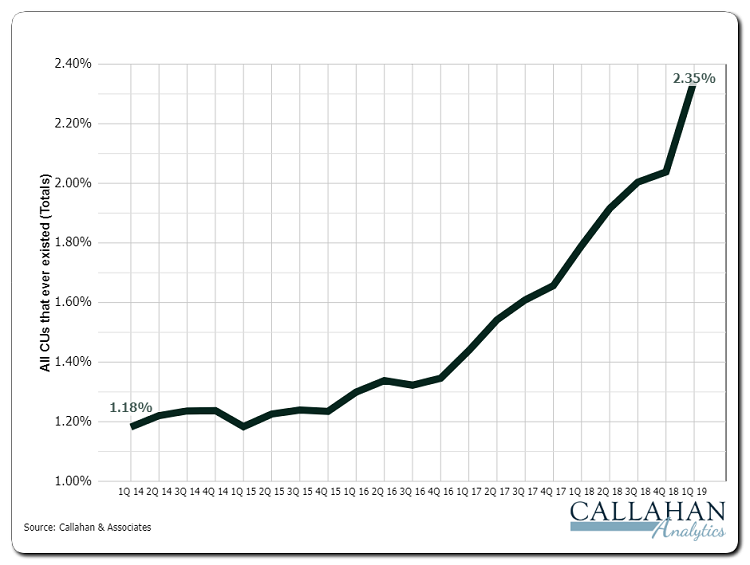

Yield On Investments

The average yield on investments rose 31 basis points from the fourth quarter of 2018, reaching 2.35% as of March 31. This is the highest level since the fourth quarter of 2009 when the average yield was 2.63%. Credit union investment earnings continue to benefit from the Fed increasing rates four times in 2018. The Fed now has signaled a change in course from its previously released estimates and is adopting a patient policy for the remainder of 2019, signaling that rates will likely be unchanged for the rest of the year.

However, the combination of growing investment balances up 12.2% from the fourth quarter and up 1.0% from one year ago coupled with an increasing concentration in shorter maturity investments will continue to drive investment income expansion up 14.9% quarterly and 28.5% year-over-year and likely push industry yields higher across the upcoming quarters.

YIELD ON INVESTMENTS

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.19

Callahan & Associates | CreditUnions.com

Yields tick higher as investments shift short.

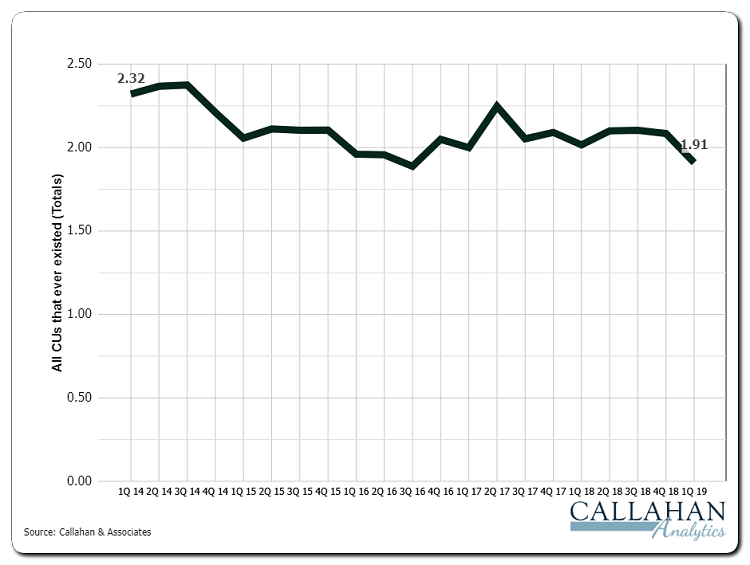

Average Life Profile

Shifting balances and notable increases in certain segments pushed down the weighted average life of all credit union investments to 1.91 years in the first quarter of 2019. Specifically, the 41.3% increase in cash and equivalents offset the growth of longer duration segments five to 10 years and greater than 10 years were up 8.9% and 9.0%, respectively to bring down the weighted average life of the industry investment portfolio.

TREND: WEIGHTED AVERAGE LIFE OF INVESTMENT PORTFOLIO (INCL. CASH)

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.19

Callahan & Associates | CreditUnions.com

Weighted average life falls as portfolios change.

Derivatives

Derivatives dropped from to $12.2 billion in December 2018 to $10.8 billion in the first quarter of 2019. The number of credit unions reporting derivative usage declined by two institutions from 70 in the fourth quarter of 2018 to 68 in the first quarter of 2019.

TOTAL NOTIONAL DERIVATIVES

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.19

Callahan & Associates | CreditUnions.com

Program participation falls slightly.

Sam Taft is the AVP of Analytics at Callahan & Associates. He also leads the business development efforts for the Trust for Credit Unions family of mutual funds, of which Callahan Financial Services (a broker dealer subsidiary of Callahan & Associates) is the distributor.