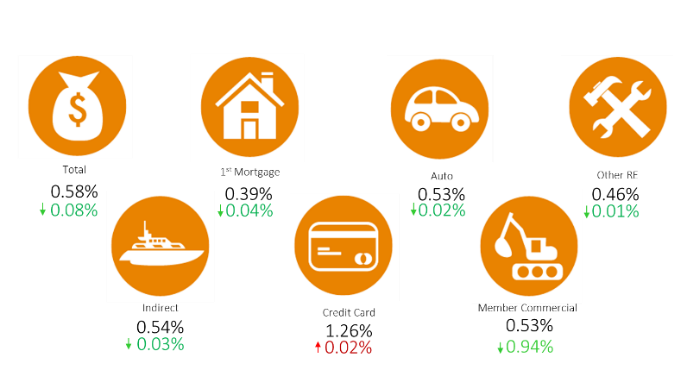

Asset quality at U.S. credit unions improved across the industry in the first quarter of 2019. Total delinquency decreased 8 basis points year-over-year to 0.58%. This represents the third consecutive year of annual decreases, and credit union delinquency is now at its lowest level since 2007.

Banks insured by the FDIC reported an average delinquency rate of 0.99% a full 41 basis points higher than the credit union average. This is all the more notable given that banks report delinquency after 90 days of nonpayment whereas credit unions report after 60 days. Also notable at credit unions is the fact delinquency is lower than one year ago in all loan products save credit cards.

ANNUAL CHANGE IN DELINQUENCY

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.19

Callahan & Associates | CreditUnions.com

Total delinquency at U.S. credit unions fell 8 basis points year-over-year as delinquency improved for all products, aside from credit cards, in the first quarter of 2019.

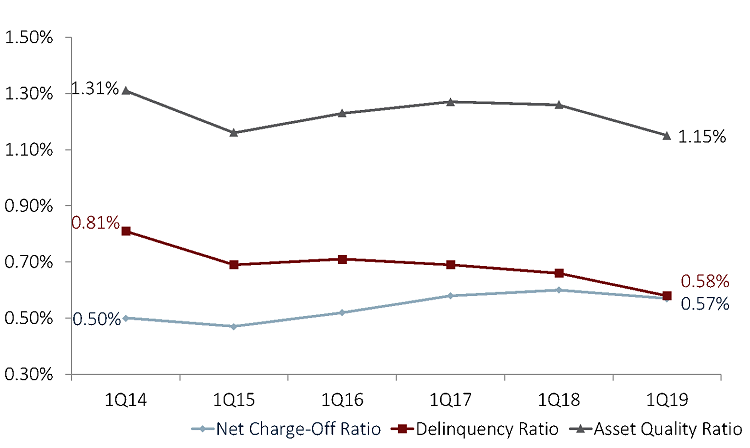

Total net charge-offs also decreased year-over-year at U.S. credit unions. They were down 3 basis points to 0.57% as of March 31, 2019. Prior to this year, a rise in credit card charge-offs drove an increase in net charge-offs for three consecutive years.

Net charge-offs at banks remained steady year-over-year at 0.50%. Although this is lower than what credit unions reported, banks have more real estate and commercial loans in their portfolios than do credit unions 72.0% versus 50.3%, respectively. These loans typically charge-off at a lower rate, which helps lead to a smaller overall percentage of charged-off loans.

The drop in both delinquency and charge-offs at U.S. credit unions has resulted in improved asset quality. The asset quality ratio which is the sum of the delinquency ratio and the net charge-off ratio was down 11 basis points annually in the first quarter of 2019. Steps credit unions have taken to improve the asset quality ratio include refining underwriting processes and payment plans to ensure members have the ability to repay, which helps reduce delinquency as well as charge-offs.

ASSET QUALITY RATIO: NET CHARGE-OFF RATIO + DELINQUENCY RATIO

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.19

Callahan & Associates | CreditUnions.com

Delinquencies and net charge-offs at credit unions have improved year-over-year. So, too, has the asset quality ratio.

Real Estate

Mirroring delinquency in the overall portfolio, delinquency for first mortgage loans improved 4 basis points year-over-year to 0.39% as of March 31. First mortgage delinquency in the first quarter has continually improved since 2011 at U.S. credit unions, and this is the lowest post-recession rate the industry has reported. Other real estate delinquency dropped 1 basis point to 0.46%.

Real estate loan charge-offs are among the lowest in the portfolio. As of March 31, 2019, first mortgage charge-offs and other real estate charge-offs for U.S. credit unions was 0.01% and 0.02%, respectively. At cooperatives nationwide, overall asset quality in real estate loans has returned to pre-recession levels and are once again among the best performing loans on the balance sheet.

ASSET QUALITY: REAL ESTATE LOANS

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.19

Callahan & Associates | CreditUnions.com

The asset quality ratio for real estate loans at credit unions nationwide is returning to pre-recession levels.

Credit Cards

Credit cards account for 5.8% of the industry’s overall loan portfolio and are the only loan product for which credit unions reported an increased delinquency rate in the first quarter. Credit card delinquency has ticked up every year over the past five years and rose a modest 2 basis points since March 31, 2018. At 1.26%, credit card delinquency is the highest of any major loan product.

Credit card net charge-offs are also on the rise. They’ve increased 1.1 percentage points in the past four years and reached 3.08% as of March 31, 2019. Total net charged-off credit card loan balances reached $1.9 billion in the first quarter and accounted for 31.8% of the $6.0 billion in total net charge-offs at U.S. credit unions. Not surprisingly, the asset quality ratio for credit cards increased 25 basis points year-over-year to 4.34%.

ASSET QUALITY: CREDIT CARDS

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.19

Callahan & Associates | CreditUnions.com

Credit card loans are the only major product for which credit unions reported an increased rate in either delinquency or net charge-offs.

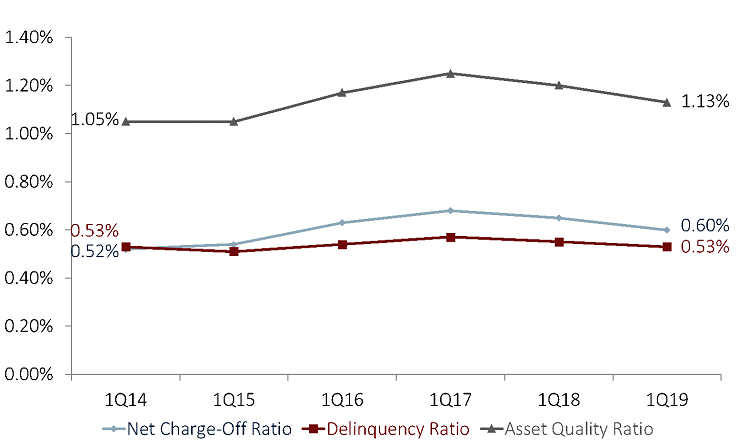

Auto

Credit unions have managed to keep auto delinquency within a 10-basis-point window since they began reporting on the metric in 2013. As of March 31, 2019, auto loan delinquency was 0.53%.

Broken out, the delinquency rate was 0.35% for new auto loans and 0.65% for used. Delinquency in the direct auto loan portfolio dropped 2 basis points year-over-year to 0.52%. And, notably, credit unions reported the lowest delinquency ever for indirect lending. It dropped 3 basis points year-over-year to 0.54% in the first quarter as credit unions worked to manage delinquency for loans originated inside the institution as well as through a third party.

Like delinquency, the net charge-off rate for new auto loans was lower than for used 0.43% versus 0.72%, respectively. Total net charge-offs for the auto portfolio decreased 5 basis points annually to 0.60%. The total asset quality ratio decreased 7 basis points year-over-year to 1.13%. This is the second consecutive year that the sum of the auto delinquency rate and the auto net charge-off rate has declined in the first quarter.

ASSET QUALITY: AUTO

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.19

Callahan & Associates | CreditUnions.com

This year represents the second consecutive year that the sum of the auto delinquency rate and the auto net charge-off rate has declined in the first quarter.

Member Commercial

Delinquency for member commercial loans decreased by the largest amount of any loan segment. It was down 94 basis points from the first quarter of 2018 to 0.53% in the first quarter of 2019. Three credit unions heavily tied into taxi medallion loans were purchased or systematically shut down, which had a dramatic effect on both commercial delinquency and net charge-off rates. Member commercial net charge-offs decreased 33 basis points to 0.08%. The total asset quality ratio for member commercial loans at U.S. credit unions dropped from 1.98% as of March 31, 2018, to 0.61% as of March 31, 2019. That’s a drop of 1.4 percentage points.

Industrywide, overall asset quality has continually improved over the past five years. Notably, the real estate market has returned to pre-recession asset quality levels. This trend coupled with credit unions’ continued success in underwriting auto loans has promoted higher loan yield over the course of the year, up 18 basis points to 4.77% as of March 31, 2019.