On Wednesday, Callahan & Associates hosted its quarterly Trendwatch webinar, an event that recaps the industry’s performance trends over the past three months as well as highlights industry success stories and areas of opportunity.

Callahan bases its analysis on data gathered through its FirstLook program, which means Trendwatch attendees have access to insight they won’t find anywhere else weeks before the official NCUA data release. This quarter’s Trendwatch was based on performance data on more than 6,000 credit unions representing more than 99% of industry assets, and more than a few exciting trends have emerged. Here are three.

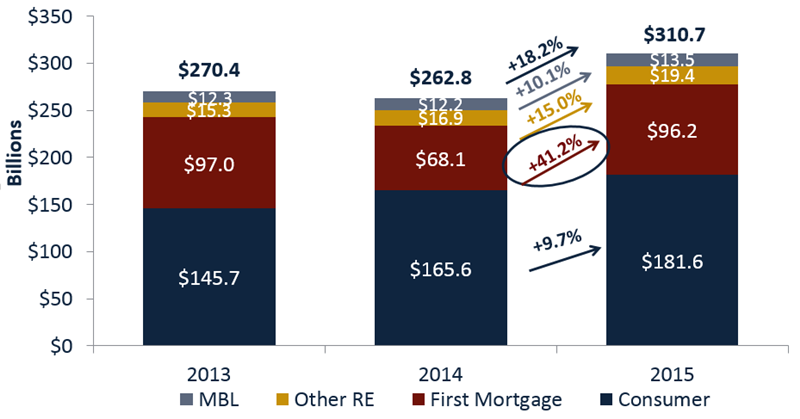

1. First mortgage originations increased 41% YOY.

First mortgage originations increased 41% YOY. That’s the highest third quarter growth rate since September 2005.

Activity in the first mortgage portfolio underpinned the overall growth of 18% in total originations, which is itself a record high for the third quarter.

YEAR-TO-DATE LOAN ORIGINATIONS

For FirstLook credit unions | Data as of 09.30.15

© Callahan & Associates | www.creditunions.com

Source: Peer-to-Peer Analytics by Callahan & Associates

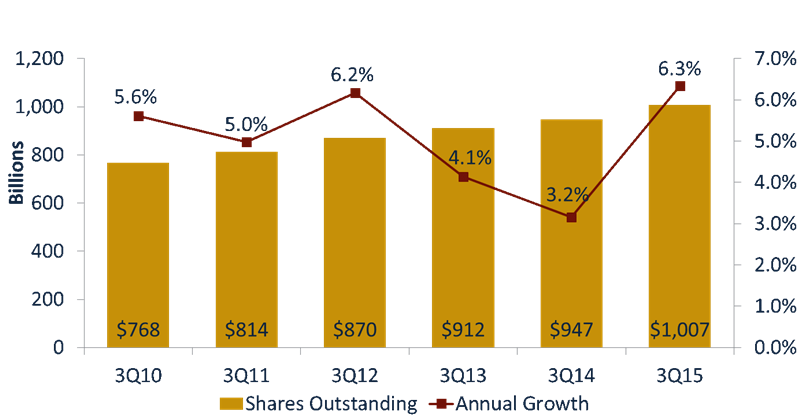

2. Total shares topped $1 trillion.

Total shares hit an all-time high of more than $1 trillion. The share growth rate was 6.3%.

SHARES OUTSTANDING AND ANNUAL GROWTH

For FirstLook credit unions | Data as of 09.30.15

© Callahan & Associates | www.creditunions.com

Source: Peer-to-Peer Analytics by Callahan & Associates

Membership, meanwhile, increased 3.7% year over year, and the industry now boasts a total of 103.6 million members.

That share growth outpaced membership growth suggests existing members are reinvesting in their credit union relationships. But share growth isn’t the only metric that underscores the industry’s strengthening relationship with its member-owners. Average member relationship increased by almost $700 year over year, and share draft penetration reached an all-time high of 55%.

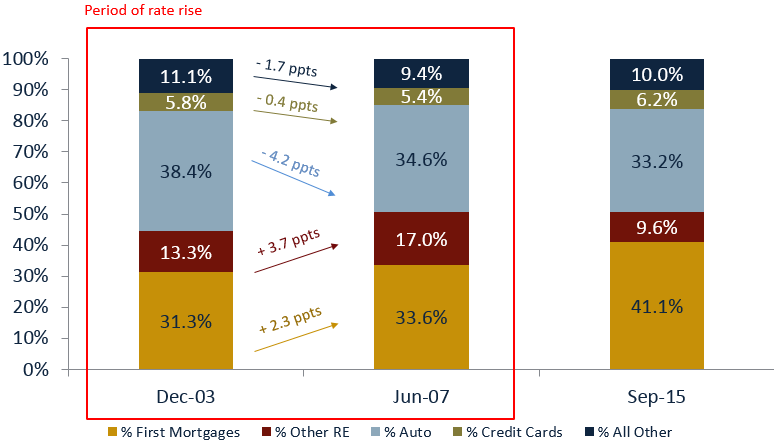

3. The credit union business model is well-positioned for a rise in interest rates.

Callahan executive vice president Jay Johnson looked at how the credit union business model shifted when the Fed last raised its short-term rate from June 2004 to June 2007.

In the loan portfolio, the concentration of first mortgages and other real estate loans increased while auto loans decreased. Fixed rates became less common in real estate loans originated, and the average yield on loans increased slightly.

In the share portfolio, higher returns meant members were more willing to lock up funds for a longer period of time. Non-core deposits increased, and share growth fell behind loan growth.

The net interest margin declined as interest expense as a percentage of average assets rose more than interest income. This is something to be prepared for in 2016, but overall, the credit union business model is well-positioned for a rise in interest rates.

LOAN COMPOSITION

For U.S. credit unions

© Callahan & Associates | www.creditunions.com

Source: Peer-to-Peer Analytics by Callahan & Associates

Don’t Miss Out!

There’s more to celebrate, but you won’t know if you don’t go. Register now for Trendwatch — Day 2.