Read the full analysis or skip to the section you want to read by clicking on the links below.

LENDING

AUTO LENDING

MORTGAGE LENDING

CREDIT CARDS

MEMBER BUSINESS LENDING

SHARES

INVESTMENTS

MEMBER RELATIONSHIPS

EARNINGS

SPECIAL SECTION: EMPLOYEE ENGAGEMENT

Real estate loan balances outstanding at credit unions increased 9.5% year-over-year to reach $456.6 billion as of June 30, 2017. First mortgages accounted for $375.7 billion of those balances outstanding and represented 82.3% of the credit union real estate lending portfolio.

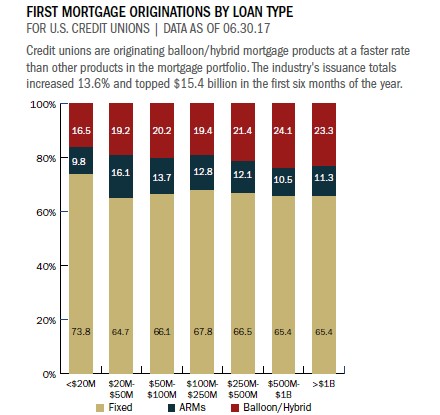

Although credit unions posted growth in all first mortgage lending products, the greatest year-over-year expansion, 13.6%, occurred in balloon/hybrid mortgage loans.

As of mid-year, 26.9% of all first mortgage loans on the industry’s balance sheet were balloon/hybrid. Fixed-rate first mortgage balances increased 10.0% annually to $218.3 billion and accounted for 58.1% of all first mortgage loans.

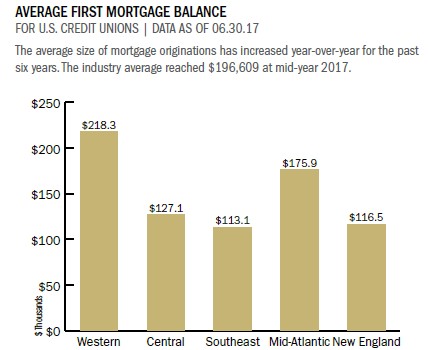

The average first mortgage origination balance has increased every year for the past six years. In second quarter 2011, first mortgage origination balances averaged $164,273. As of second quarter 2017, the average balance was $196,609. That’s an increase of more than $40,000.

Credit unions in NCUA’s Western Region led the industry with an average first mortgage balance of $267,936. That’s almost $50,000 more than the Mid-Atlantic Region, which comes in at No. 2 with an average of $219,305.

Year-to-date first mortgage sales to the secondary market dropped to $22.8 billion. That’s a 3.6% decline since June 30, 2016. As a percentage of first mortgage originations, sales to the secondary market also declined. Credit unions sold 33.8% of first mortgage originations as of June 30. That’s down 3.8 percentage points from June 30, 2015, and down 18 percentage points from June 30, 2013. Credit unions with more than $1 billion in assets sold 35.8% of their first mortgage originations. By comparison, credit unions with $20 million or less in assets sold only 11.5%.

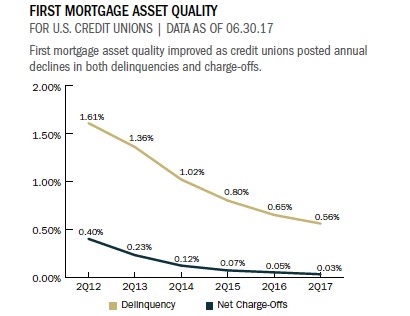

First mortgage delinquency improved across the industry. The industry’s second quarter average of 0.56% is a 9-basis-point decrease over second quarter 2016. First mortgage charge-offs also improved, falling 2 basis points year-over- year to 0.03%.

Make The Most Of Mortgage Market Data

Leveraging HMDA data, MortgageAnalyzer helps credit unions identify market leaders and analyze their performance against other credit unions, banks, and mortgage lenders.

![]()

Click the graphs below to enlarge and then continue reading to see how New York University FCU is helping members buy homes in one of the nation’s priciest housing markets.

Sales to the secondary market dropped 3.6% over the past year to $22.8 billion. Credit unions with more than $1 billion in assets sold 35.8% of total first mortgage originations in the second quarter of 2017.

CASE STUDY

NEW YORK UNIVERSITY CREDIT UNION

New York University Federal Credit Union serves one of the nation’s priciest housing markets, but the Empire State cooperative has developed ways to help members buy homes.

At the $22 million credit union, homeowner education, flexible but responsible terms, and down payment assistance are all tools that help members who will have more mortgage than salary if they find even a reasonably priced home in the Big Apple.

Salaries for members at NYUFCU range from modestly paid service workers to professors making $1 million a year. Mira Ness, the credit union’s chief executive since 2006, says the credit union never finances less than $150,000 for a home and that a typical transaction is more along the lines of the $250,000 one-bedroom apartment the credit union just financed in the Bronx.

NYUFCU also recently financed $2 million for a 1,000-square-foot condo that went for $3.18 million in the Lower East Side and has made loans up to $3 million. NYUFCU requires a 10% down payment for a home loan. To help potential borrowers get there, the credit union participates in a first-time homebuyer program with the Federal Home Loan Bank. The class meets for six hours and covers the basics. In return, successful participants who save approximately $1,900 over 10 to 12 months receive a match that brings the total up to $8,000.

Ness says 20 to 25 potential homebuyers a year participate, and the lending program helped the credit union sustain its relationship with NYU itself.

We’ve been around for 35 years, and the university is still behind us, Ness says. We just moved into a new space, and we’re happy with our relationship with the university’s new president.

Read The Whole Story

Strategy Performance 2Q 2017

Credit unions are indeed having an outstanding 2017 right on the heels of a very strong 2016 and 2015. Eliminating barriers and connecting with members distinguishes credit unions from other financial institutions and makes the movement stronger than it’s ever been. Learn what the industry’s most successful credit unions are doing in this issue of Strategy Performance.